AFE vs. JIB: Why Working Interest Owners See Cost Differences After Approval

Summary

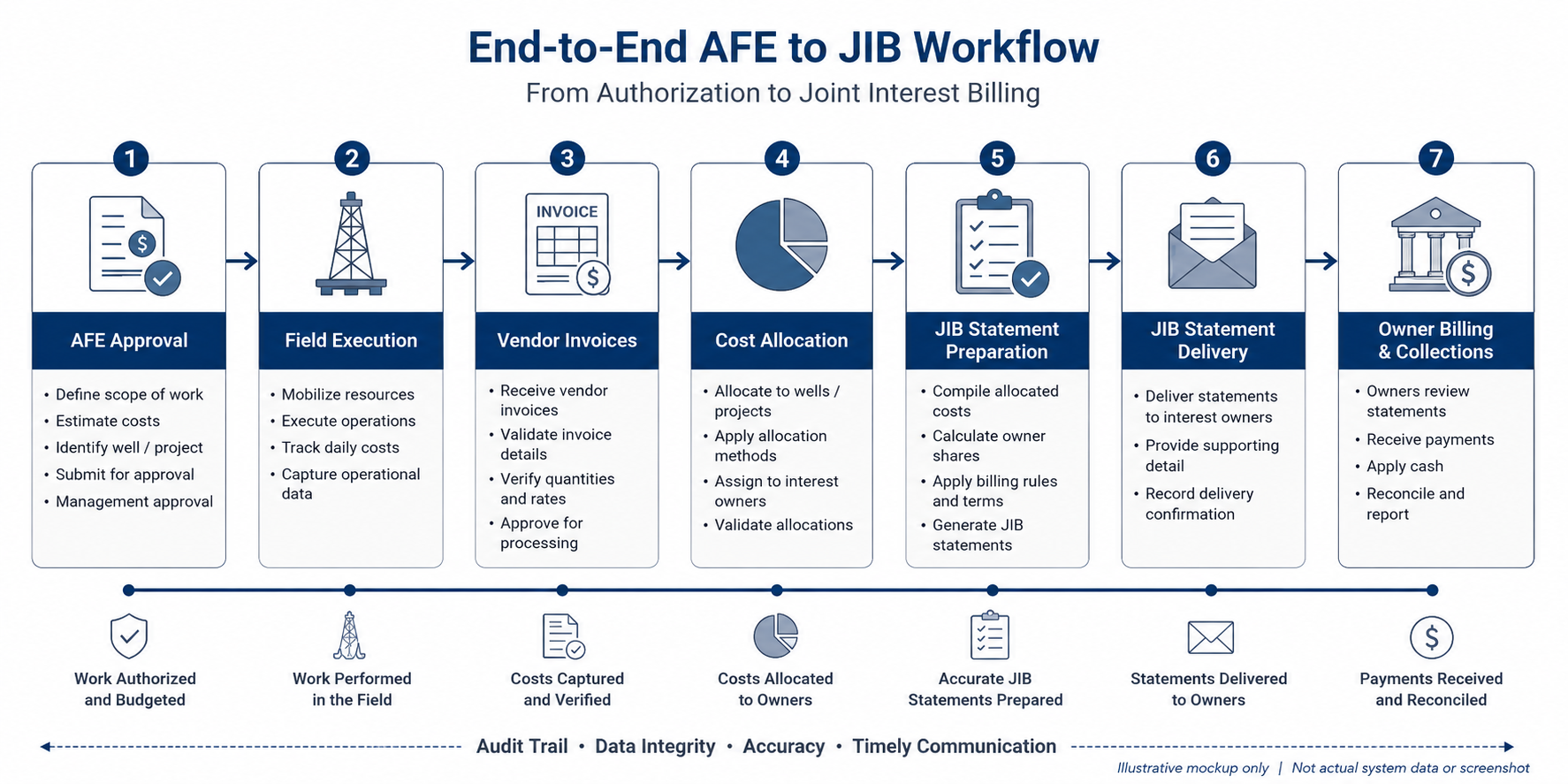

×AFE Is the Plan, JIB Is the Bill

For working interest owners, one of the most common questions after approving an AFE is simple: “Why is my JIB higher than the amount I approved?” The answer is that an AFE, or Authorization for Expenditure, is usually a cost estimate prepared before work begins, while a JIB, or Joint Interest Billing statement, reflects actual costs allocated after work is performed. These two documents are connected, but they do not serve the same purpose.

An AFE gives non-operating working interest owners visibility into expected costs before capital is committed. It may cover drilling, completion, workover activity, facilities, equipment, labor, or other project costs. A JIB is issued later and allocates the working interest owner’s share of actual expenses based on the joint operating agreement and ownership percentage.

That timing difference matters. The AFE is based on assumptions, vendor quotes, expected field conditions, planned scope, and estimated timing. The JIB is based on invoices, field activity, cost coding, overhead allocations, and actual operational decisions made during execution.

The Basic Formula Behind JIB Charges

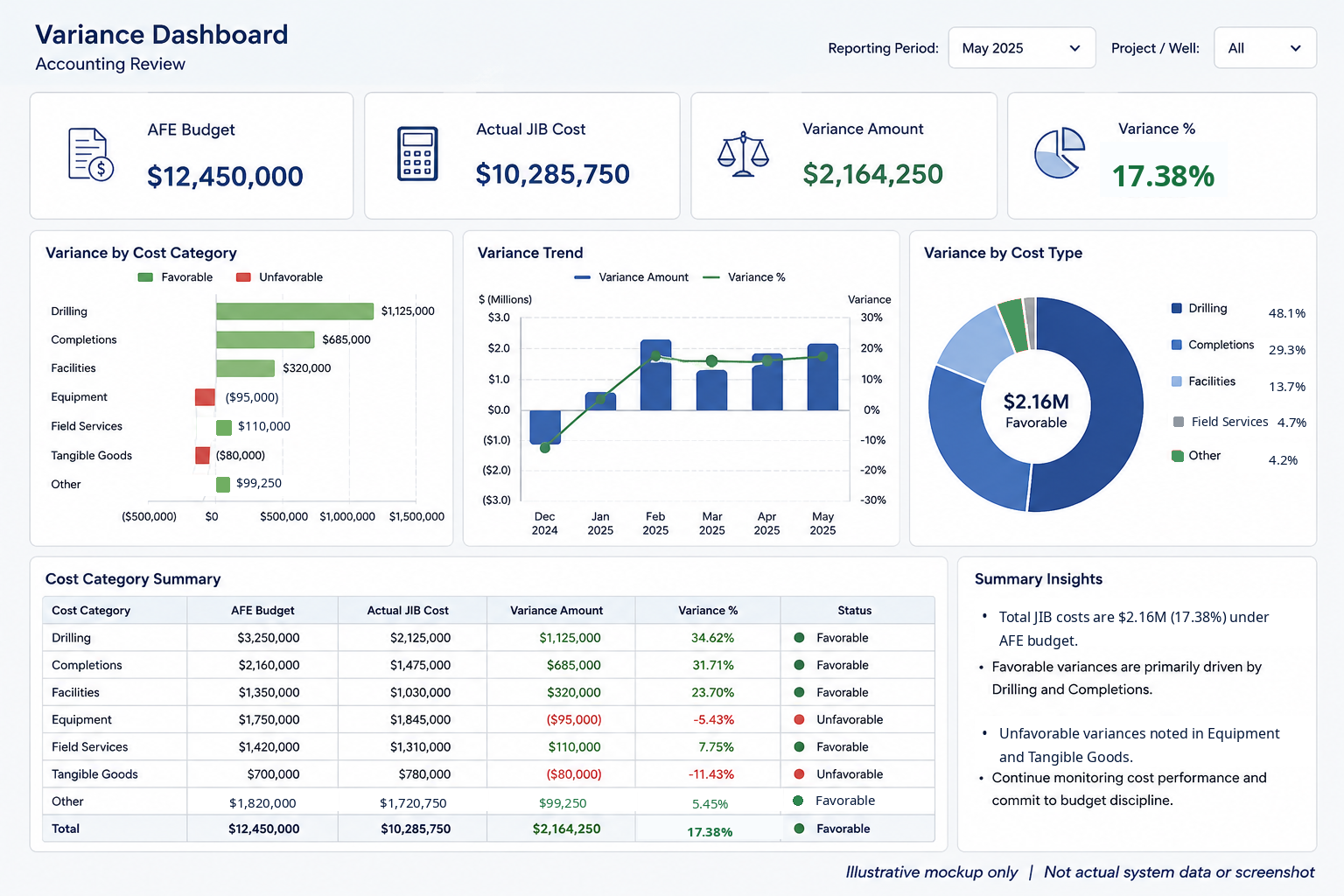

A simple formula helps explain why working interest owners may see a different number on the JIB than they expected from the AFE. The operator records the gross project cost, then allocates that cost according to each owner’s working interest percentage. If the actual cost changes, the owner’s share changes as well.

The calculation can be stated as: Working Interest Owner JIB Charge = Gross Actual Cost × Working Interest Percentage. For example, assume a well completion AFE estimated total gross costs of $1,200,000. A working interest owner with a 12.5% working interest would expect a share of $1,200,000 × 12.5% = $150,000.

If the final actual gross cost becomes $1,320,000, the owner’s allocated JIB charge becomes $1,320,000 × 12.5% = $165,000. The difference is $165,000 - $150,000 = $15,000. The owner did not necessarily receive an incorrect bill; the project may have simply cost more than originally estimated.

The key question is not only whether the JIB amount is higher. The more useful question is whether the difference is supported by proper cost detail, coding, approvals, field activity, and operating documentation. That is where a structured review process becomes important.

A Simple Variance Formula Owners Can Use

Working interest owners can use a basic variance calculation before raising a question with the operator. This makes the review more objective and helps separate normal cost movement from charges that may require follow-up. It also creates a better conversation because the owner can ask about a specific variance instead of questioning the entire statement.

The review can use two simple formulas: JIB Variance = Actual JIB Charge - Expected AFE Share and JIB Variance Percentage = JIB Variance ÷ Expected AFE Share × 100%. Using the earlier example, the variance is $15,000, and the variance percentage is $15,000 ÷ $150,000 × 100% = 10%.

A 10% variance may be reasonable in some field conditions, but it may require explanation if the project scope was expected to remain tightly controlled. Owners should look at both the dollar variance and the percentage variance because a small percentage on a large project can still represent a meaningful cash flow impact.

Why Cost Differences Happen After Approval

Cost differences often happen because the AFE is prepared before the operator has complete certainty. Field conditions can change, vendor pricing can shift, timing can affect labor or equipment costs, and operational decisions may be adjusted to protect safety, production, or asset value. In drilling, completion, and workover activity, even a well-planned project can move outside the original estimate.

Another common reason is scope change. An AFE may approve a defined work program, but actual execution may require additional equipment, remedial work, extra trucking, added water handling, or extended rental time. These changes may be valid, but they should be visible enough for working interest owners to understand why the cost moved.

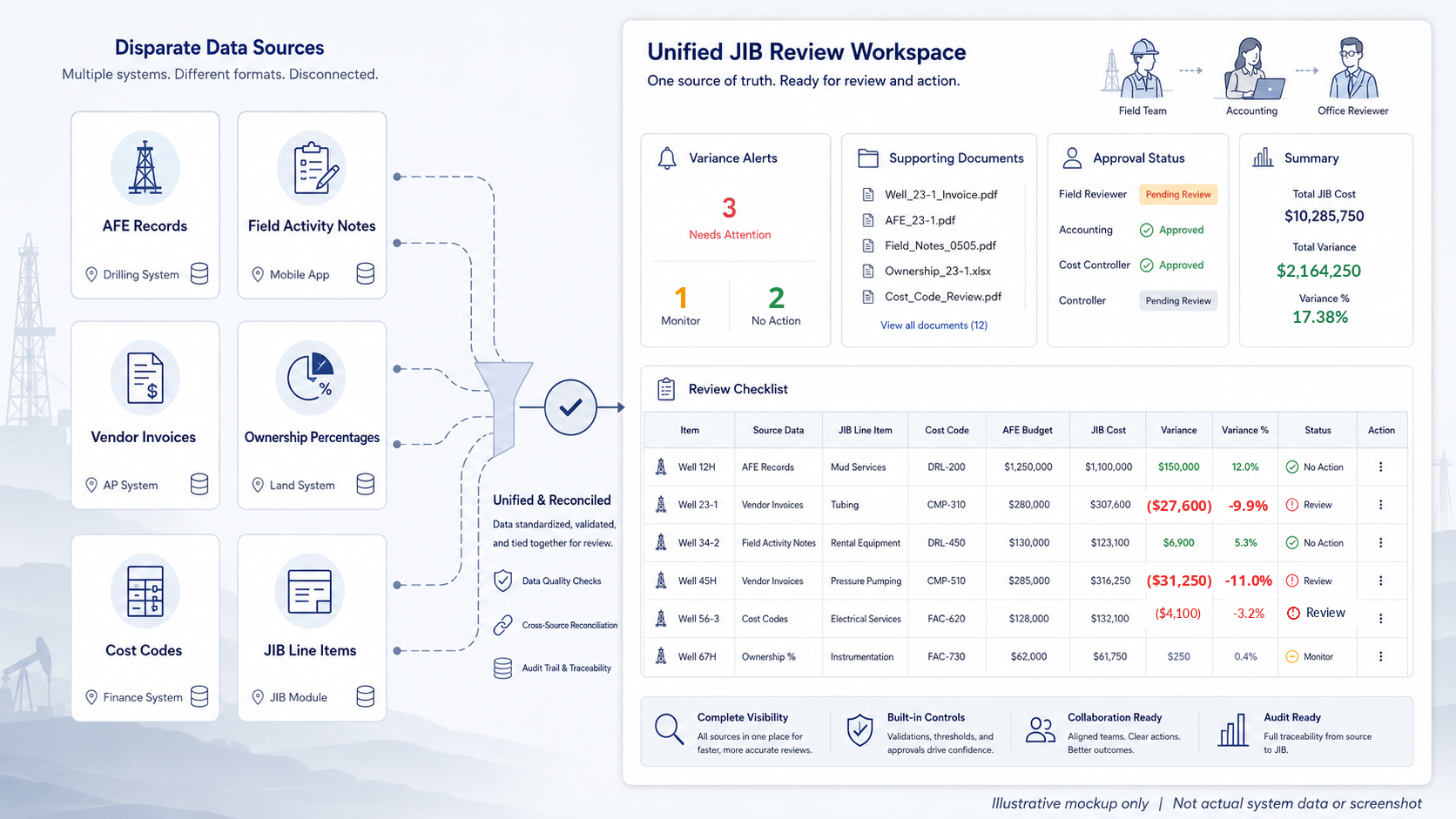

Cost differences can also come from coding and allocation issues. A charge may be legitimate but assigned to the wrong well, cost center, project phase, or owner group. This is why working interest owners should not only compare the total amount, but also review line-item categories, cost descriptions, service dates, and whether the charge belongs to the project they approved.

Common sources of AFE-to-JIB variance include:

Field conditions that differ from the original plan

Vendor price changes or equipment availability issues

Added trucking, disposal, rental, or service time

Scope changes needed during execution

Costs coded to the wrong well, phase, or category

Ownership or allocation records that need review

When a Higher JIB May Be Reasonable

Consider a non-operating owner that approved a $900,000 gross AFE for a recompletion project. The owner has a 20% working interest, so the expected share is $900,000 × 20% = $180,000. When the JIB arrives, the gross project cost is $972,000, making the owner’s share $972,000 × 20% = $194,400.

At first glance, the owner sees a $14,400 increase and may assume something went wrong. After reviewing the cost detail, the increase comes from additional wireline work, extra disposal costs, and longer equipment rental due to weather delays. If the operator provides clear documentation and the charges align with actual field conditions, the higher JIB may be reasonable.

The same increase would look very different if the detail were vague. If the statement only showed broad categories such as “services” or “operations expense,” the owner would have less confidence in the billing. The issue is not only the cost increase, but the quality of explanation behind the increase.

Where Owners Should Look First

Working interest owners should begin by comparing the approved AFE categories against the JIB line items. The goal is not to challenge every difference, but to identify charges that fall outside the expected scope, timing, or project category. This is especially important when a project includes multiple wells, multiple cost centers, or several phases of work.

Useful review questions include whether the charge belongs to the correct well, whether the service date matches the project timeline, and whether the cost category matches the approved activity. Owners should also check whether overhead, supervision, transportation, disposal, materials, or third-party services are being billed consistently with the joint operating agreement. A structured review helps owners avoid both overpaying and delaying valid payments.

The strongest review process is usually built around exceptions. Instead of manually rereading every line, owners can focus on large variances, unfamiliar vendors, unusual cost categories, duplicate-looking charges, or costs billed after the expected project window. This approach makes the review faster and more practical for teams managing multiple wells or operators.

Owners should prioritize review items such as:

Large dollar or percentage variances

Charges outside the approved AFE category

Costs billed after the expected project window

Unfamiliar vendors or vague cost descriptions

Duplicate-looking invoices or repeated charges

Costs that appear to belong to another well or phase

Not Every Difference Is an Error

A higher JIB does not automatically mean the operator billed incorrectly. Oil and gas operations involve changing field conditions, and some cost movement is normal. Working interest owners should avoid treating every variance as a dispute because that can slow payment, strain operator relationships, and create unnecessary administrative work.

At the same time, owners should not approve JIB charges without a clear review process. A difference may point to an incorrect allocation, duplicate invoice, miscoded expense, unauthorized scope expansion, or unclear supporting documentation. The practical goal is to separate valid operational variance from preventable billing error.

A balanced review protects both sides. Operators receive payment faster when owners understand the reason behind cost changes. Working interest owners gain better cost control when they can see how approved budgets convert into actual charges.

Better Data Reduces JIB Questions

Many JIB questions come from disconnected information. The AFE may live in one system, field activity notes in another, vendor invoices in another, and JIB statements in yet another. When the owner receives a bill, the cost may be valid, but the supporting story is difficult to trace.

Better data structure helps reduce confusion. When AFE categories, cost codes, project phases, ownership percentages, vendor invoices, and JIB line items are connected, owners can review charges with more confidence. Operators also benefit because clearer records reduce back-and-forth questions before payment.

For working interest owners, the most valuable system is not just one that stores statements. It should help compare approved estimates against actual charges, flag meaningful variances, keep supporting documents organized, and make the review process repeatable. That visibility turns JIB review from a reactive dispute process into a controlled financial workflow.

A Practical Review Example

A working interest owner receives a JIB statement with a $62,000 charge for a project that had an expected owner share of $54,000. The variance is $8,000, or approximately 14.8%. Instead of immediately disputing the full amount, the owner compares the JIB line items against the approved AFE categories.

The review shows that $4,500 relates to additional disposal costs, $2,000 relates to rental equipment used for three extra days, and $1,500 relates to a vendor charge that appears under the wrong cost category. The first two items may be valid if they match field records and invoices. The third item may require clarification or correction because the issue is not necessarily the amount, but how the cost was coded.

This kind of review gives the owner a stronger position. The owner can approve the supported charges, ask a focused question about the questionable item, and avoid delaying the entire payment cycle. The operator also receives a clearer request and can respond faster.

Where Petrofly Can Help

Petrofly can help oil and gas teams make AFE-to-JIB differences easier to review by connecting approved budgets, actual JIB charges, ownership data, cost categories, supporting documents, and payment status in one workflow.

Key areas include:

AFE-to-JIB visibility: Compare approved estimates with actual charges and supporting cost detail.

Variance review: Focus on meaningful differences by well, project, cost category, or owner share.

Document connection: Keep invoices, approval context, cost notes, and payment status close to the related charge.

Ownership and allocation support: Connect working interest, effective dates, and owner records to cost allocation.

Cloud-based access: Give accounting, operations, and management users a shared review view without relying on scattered files.

Flexible setup: Start with AFE-to-JIB review first, then adjust fields, reports, variance views, and approval steps around the team’s actual workflow.

Dedicated support: Get help with setup, configuration, data organization, workflow refinements, and post-go-live questions when cost differences need clarification.

The value is not adding another review layer. It is making cost differences easier to explain, document, and resolve before payment questions slow the process.

Practical Takeaway

AFE and JIB differences are normal, but unexplained differences create risk. Working interest owners should expect some movement between approved estimates and actual charges, especially when field conditions change. What matters most is whether the JIB provides enough detail to connect the final charge back to the approved scope, actual work, and ownership share.

A strong review process does not need to be complicated. Owners can use simple formulas, variance thresholds, cost-category checks, and supporting documentation to decide when a charge is reasonable and when it needs follow-up. The better the connection between AFE data, field activity, invoices, and JIB statements, the easier it becomes to control costs before payment.

To discuss how a more connected AFE-to-JIB review workflow could support clearer payment decisions, contact our team for a focused conversation.