Oil and Gas Cash Calls: What Working Interest Owners Should Review Before Paying

Summary

×Start With Funding Exposure

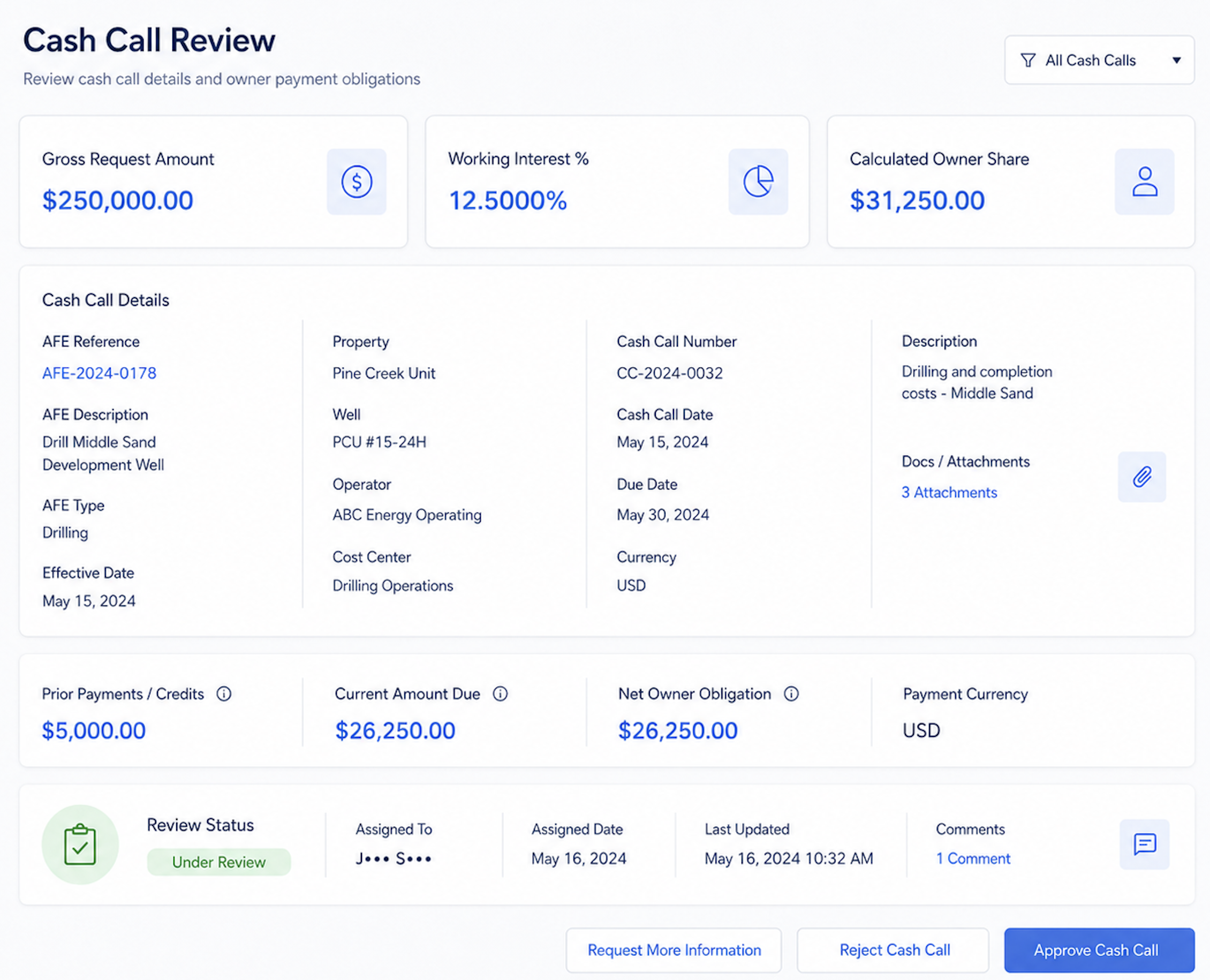

For working interest owners, a cash call is not the same as a final cost statement. It is usually a request for funding based on expected project spending, operator cash needs, or near-term field activity. The actual costs may appear later through JIB statements, and those final allocated charges may not match the cash call amount exactly.

The first review step is to check the owner’s expected share using gross cash call amount × working interest percentage. If the operator issues a $500,000 gross cash call and the owner has a 12% working interest, the expected owner share is $60,000. That confirms the basic math, but it does not prove that the request belongs to the right AFE, uses the correct ownership percentage, or accounts for previous funding.

This is why cash call review should focus on exposure, not only payment timing. A request may be valid, but the owner still needs to know whether it fits the approved scope, current funding position, and later reconciliation path. Without that context, a payment can be made on time but become difficult to explain when the related JIB statement arrives.

Compare the Request With AFE Exposure

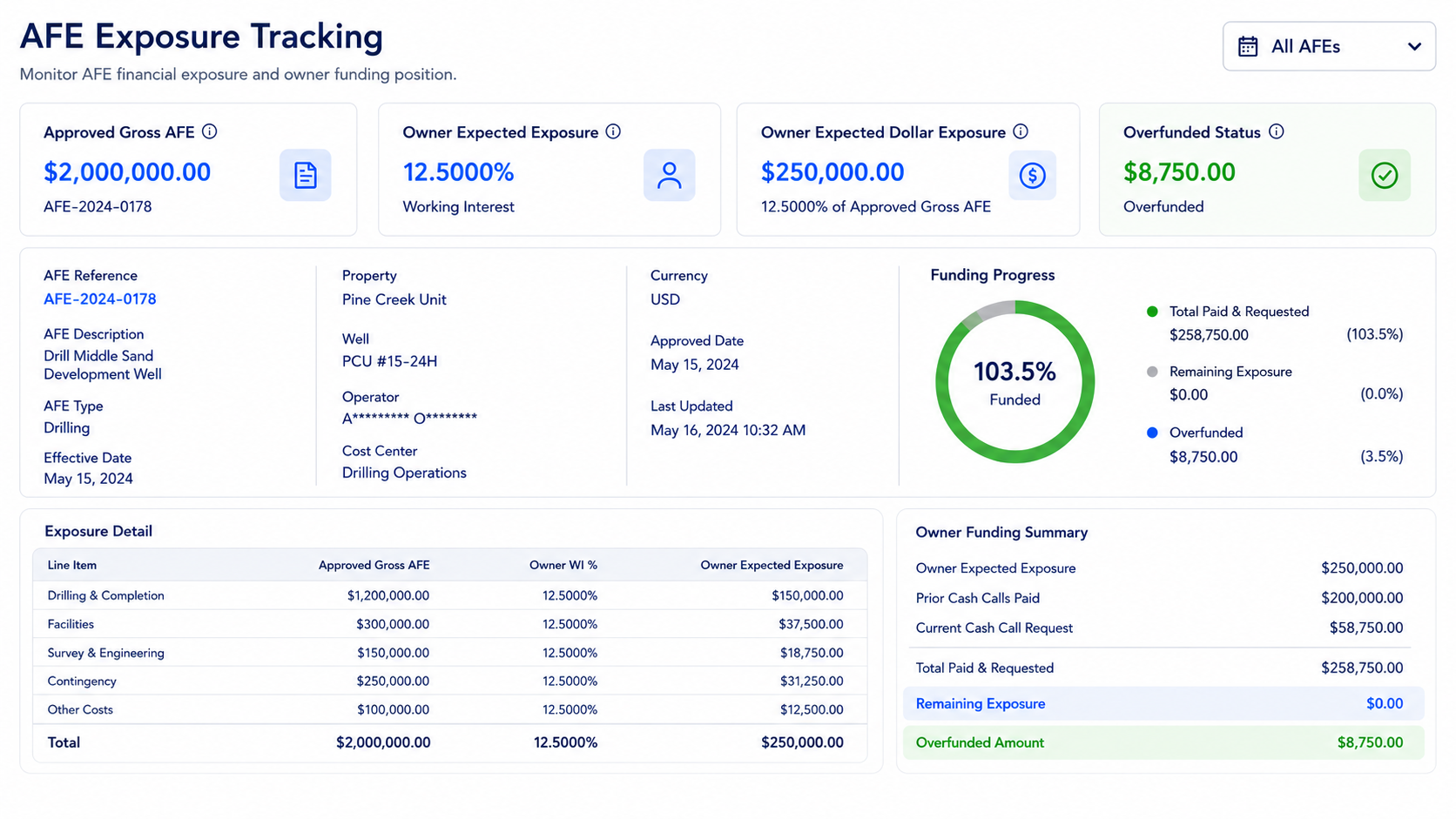

The approved AFE gives the owner a baseline for expected capital exposure. It does not guarantee the final cost, but it shows what was originally authorized and what the owner agreed to fund. When a cash call arrives, the reviewer should compare the request with the owner’s expected AFE exposure before approving payment.

The owner’s expected exposure can be estimated as approved gross AFE × working interest percentage. If an approved gross AFE is $1,200,000 and the owner has a 10% working interest, the expected exposure is $120,000. If the operator sends a first cash call for $70,000, the request may be reasonable because it remains below the owner’s approved share.

The review changes when cumulative funding exceeds that baseline. If a second cash call for $65,000 arrives later, cumulative funding becomes $135,000, which is $15,000 above the original expected exposure. That does not automatically mean the operator is wrong, but the request should no longer be treated as a routine payment item.

Before paying an amount above expected exposure, the owner should check:

Is there a revised AFE or documented scope change?

Is the excess tied to a known cost overrun?

Is the request funding future work or costs already incurred?

Will the excess appear in later JIB detail?

Is any portion expected to become a credit or prepaid balance?

Do Not Review the Current Request Alone

A common mistake is checking only the current cash call amount. Cash call review is cumulative, so the current request only makes sense when compared with what has already been paid for the same AFE, well, lease, or project. A request that looks reasonable by itself may become questionable once prior funding is included.

A practical check is owner AFE exposure minus prior cash calls paid. If the owner’s expected exposure is $150,000 and prior cash calls total $95,000, the remaining expected exposure is $55,000. A new request for $40,000 keeps total funding within the expected range, while a new request for $75,000 pushes cumulative funding to $170,000, or $20,000 above expected exposure.

That difference should be classified before payment. It may represent a revised scope item, timing difference, cost overrun, advance funding need, prior balance issue, or unsupported variance. Each explanation leads to a different follow-up, so the reviewer should not treat all overages the same way.

Validate Ownership and Participation

Cash call accuracy depends on the correct working interest percentage. Ownership may differ by well, lease, project, formation, effective date, or participation election. A non-operator may participate in one AFE but not another, or may have a different share for a workover than for routine operating activity.

The expected amount due should be based on gross request × correct project-level working interest. If the gross request is $600,000, the difference between 8% and 9.5% ownership is meaningful. At 8%, the owner share is $48,000; at 9.5%, it is $57,000, creating a $9,000 difference on one request.

The reviewer should confirm that the operator’s percentage matches the owner’s internal record for the correct asset, project, and period. This is especially important after acquisitions, divestitures, ownership deck updates, non-consent decisions, or changes in project participation. A cash call can look mathematically correct while still using the wrong participation basis.

Key ownership checks include:

Does the percentage match the correct well, lease, or project?

Does the effective date apply to the cash call period?

Is the owner participating in this specific AFE or activity?

Does the operator’s calculation match the internal ownership record?

Are any non-consent or partial participation issues involved?

Separate Advance Funding From JIB Cost

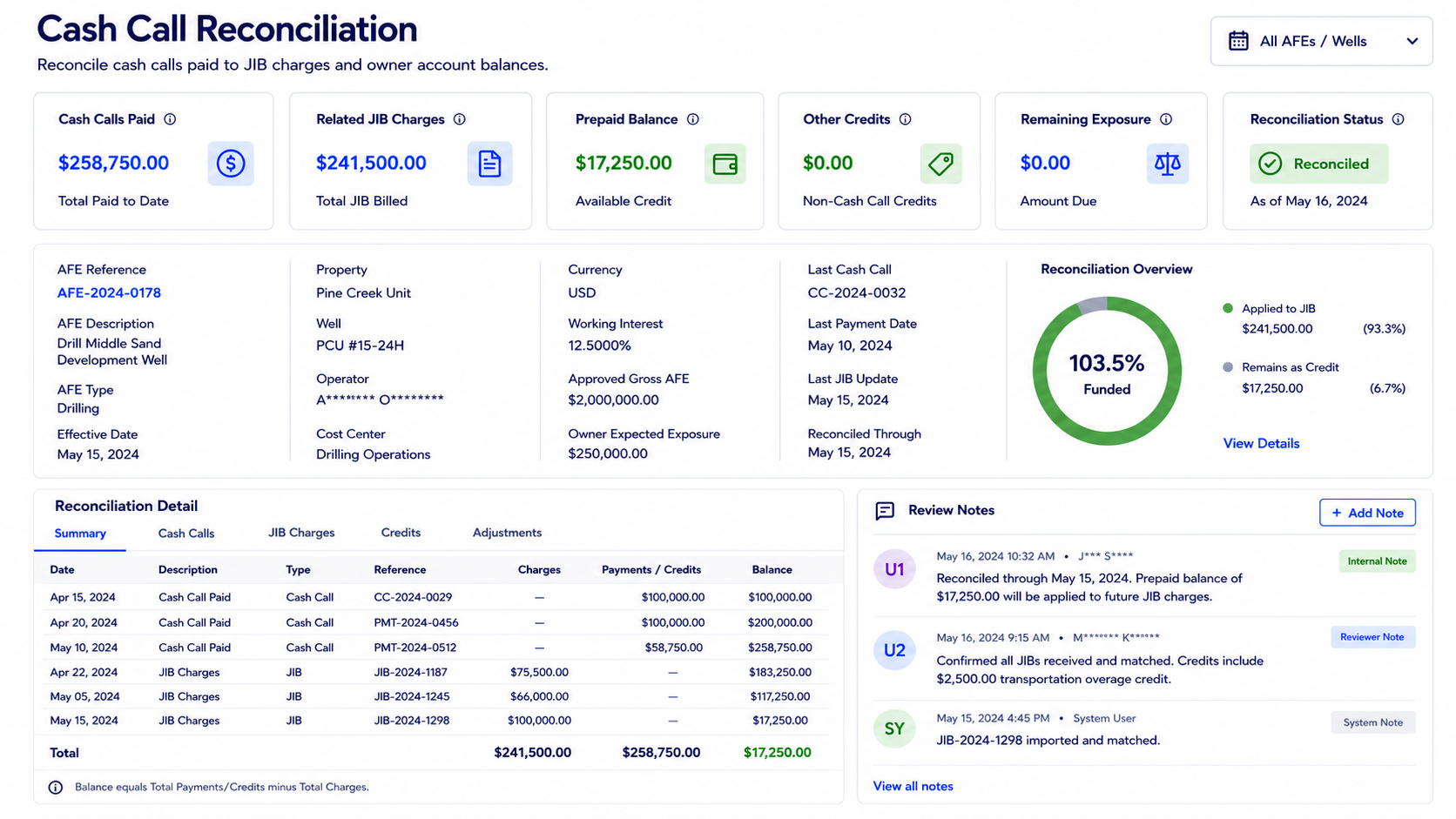

Cash calls and JIB statements are related, but they are not the same control point. A cash call may fund estimated spending before costs are finalized. A JIB statement usually reflects actual allocated costs after the operator records, classifies, and bills the charges. Maintaining a rigorous reconciliation process between these two fiscal phases allows non-operating partners to track capital efficiency more reliably, improving variance transparency while reducing the administrative frictions often found in joint venture accounting cycles.

This creates a reconciliation issue. If the owner pays $100,000 in cash calls and later receives $92,000 in related JIB charges, the $8,000 difference may represent a prepaid balance, timing difference, future billing item, or credit still to be applied. The difference is not automatically an error, but it should remain visible and explainable.

The reverse can also happen. If related JIB charges later total $115,000 against $100,000 in prior cash calls, the owner may owe an additional $15,000, assuming the charges are supported and correctly allocated. The important point is that the team should be able to trace what happened to the money after it was paid.

Review Operator Support Before Payment

A cash call should provide enough support for the owner to understand why funds are needed. The level of support may vary by operator and project, but the request should usually identify the AFE, well or project, gross amount, ownership basis, due date, and purpose of funding. If the amount is outside expected exposure, the support should explain why.

For example, “additional work required” is not as useful as “additional fishing operations added three rig days and increased the gross estimate by $180,000.” The second explanation gives the owner something to evaluate and later compare against JIB detail. A vague explanation may be acceptable for a small timing difference, but it is usually not enough for a material overrun or disputed participation basis.

The owner should preserve operator explanations with the cash call record. If the same issue appears later during JIB review, the team should not have to search old email threads to remember why the payment was approved. The review record should show what was requested, what support was provided, what questions were raised, and what decision was made.

Use Materiality Before Delaying Payment

Not every issue should delay payment. A minor support gap on a routine item may be paid with a note, while a material AFE overrun or ownership mismatch may need clarification before funds are released. Materiality helps the team avoid both overreacting to small issues and under-reviewing large ones.

For example, if the owner’s expected remaining exposure is $55,000 and the operator requests $58,000, the $3,000 difference may be handled with a note depending on company policy and project size. If the request is $85,000, the $30,000 difference should probably trigger a clearer operator explanation, revised AFE support, or management review before payment.

A practical policy may classify requests as:

Routine: within expected exposure and supported

Needs note: minor issue, low risk, payment can proceed

Needs backup: support missing or incomplete

Needs clarification: ownership, AFE, or timing does not match records

Hold or escalate: material variance unresolved before payment

How a Connected Workflow Helps

Software can help. Here’s how Petrofly does it. Cash call review becomes difficult when AFE approvals, ownership records, prior cash calls, payment notes, JIB statements, and operator explanations are managed in different places. Petrofly brings those records into one connected oil and gas workflow so working interest owners can review funding requests with clearer context and less manual reconstruction.

For cash call review, Petrofly can help teams:

Link cash calls to all related records in one system.

Review share, funding, exposure, variances, questions without spreadsheets.

Track cash calls vs AFE to see routine, overfunded, or exposure status.

Keep operator explanations, review notes, approvals, and support files attached to the same record for later JIB review.

Compare cash calls, JIB, credits, prepaids, and unreconciled amounts.

Configure fields, review steps, reports, and status labels to fit each customer’s working interest review process.

Cloud access, simple user experience, and post-launch support.

The practical value is that cash calls, AFE exposure, ownership basis, prior payments, documents, review comments, payment status, and JIB reconciliation can be handled within one system. For working interest owners, this reduces time spent searching across disconnected records and makes each funding decision easier to calculate, explain, and revisit.

Test the Review Before Payment

A strong cash call process should be tested before the payment deadline. The team should take a recent cash call and ask whether the full funding story can be reconstructed quickly. If the answer requires searching emails, folders, spreadsheets, and accounting exports, the process is probably carrying avoidable risk.

Useful test questions include:

Can the team identify the correct AFE, well, lease, or project?

Can the owner share be recalculated from gross amount and working interest percentage?

Can prior cash calls be reviewed for the same project?

Can remaining AFE exposure be calculated before payment?

Can operator support be tied to the payment decision?

Can the cash call later be matched against JIB charges or prepaid balance?

Cash call review is not about slowing down every payment. It is about knowing whether the request is supported, whether exposure is still reasonable, and whether the payment can be reconciled later. When those pieces are clear, working interest owners can fund legitimate requests with more confidence and catch material issues earlier.

To discuss how Petrofly can support a more controlled cash call review workflow, contact our team for a focused conversation. Try these cash call review steps in a free Petrofly demo. Engaging with this integrated tracking tool provides non-operating partners and joint venture teams with a more structured methodology to evaluate funding requests against approved capital budgets, helping organizations optimize working capital deployment and improve financial communication with project operators.