Generic Accounting Software vs. Oil and Gas Accounting Software: What Working Interest Owners Should Know

Summary

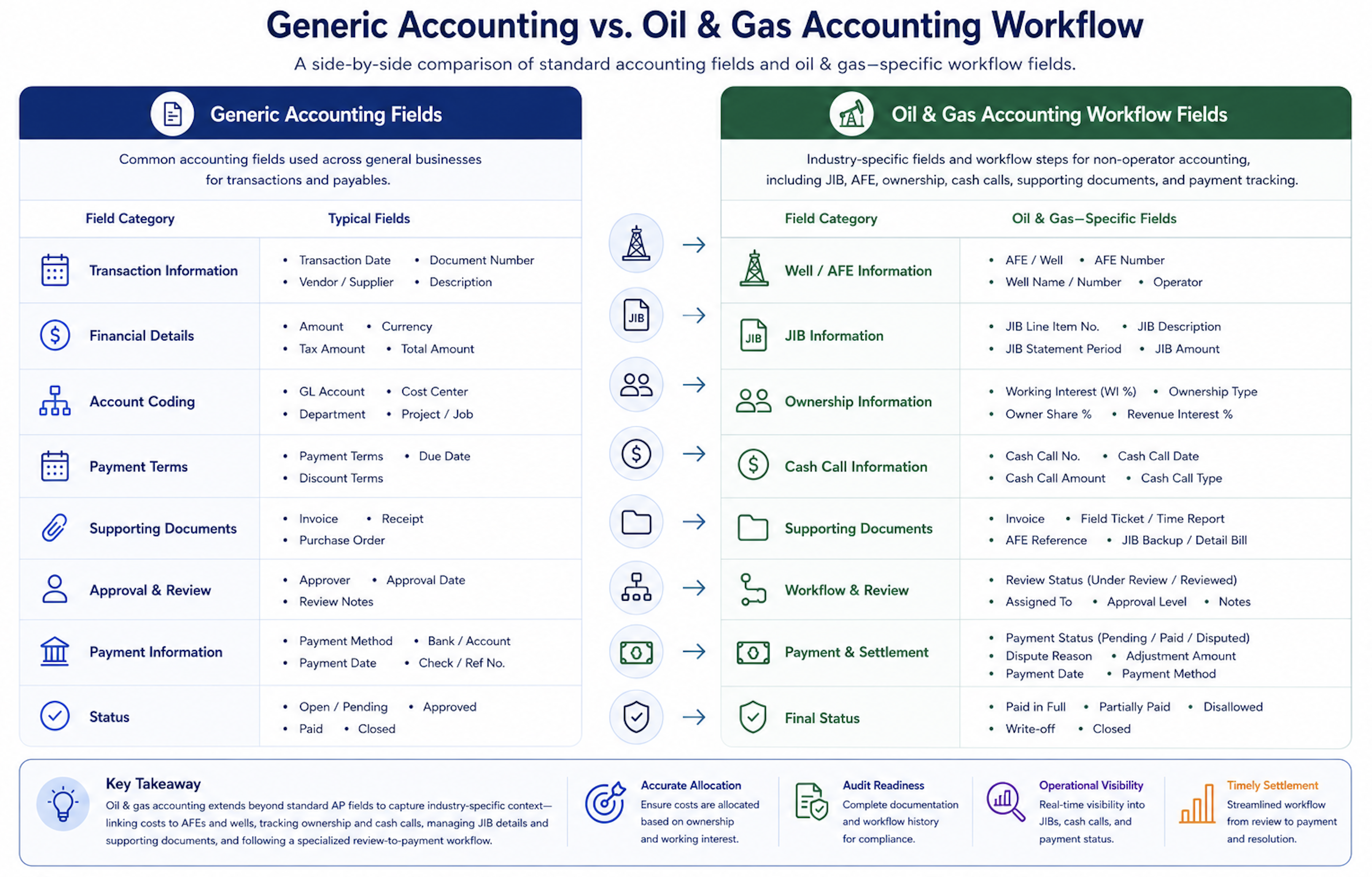

×The Difference Starts With Operating Context

Generic accounting software is usually designed to record transactions, categorize expenses, manage invoices, and support standard financial reporting. Those functions are useful, but they may not be enough when a working interest owner needs to review operator-issued JIB statements, cash calls, AFE exposure, ownership percentages, credits, adjustments, and supporting documents. Oil and gas accounting requires operating context, not only accounting entries.

For example, a generic accounting tool may record that $25,000 was paid to an operator. It may even categorize the payment as an operating expense or project cost. But it may not show whether the amount came from a JIB statement, a cash call, a workover charge, an AFE overrun, or a prior-period rebill. Without that context, the payment is recorded but not fully understood.

Working interest owners need to know more than what was paid. They need to know which operator billed the charge, which well or lease it belongs to, which ownership percentage was used, which documents support it, whether prior cash calls were applied, and whether the item remains open for review. That is the main difference between basic accounting and oil-and-gas-specific accounting workflow.

JIB Statements Need More Than Expense Categories

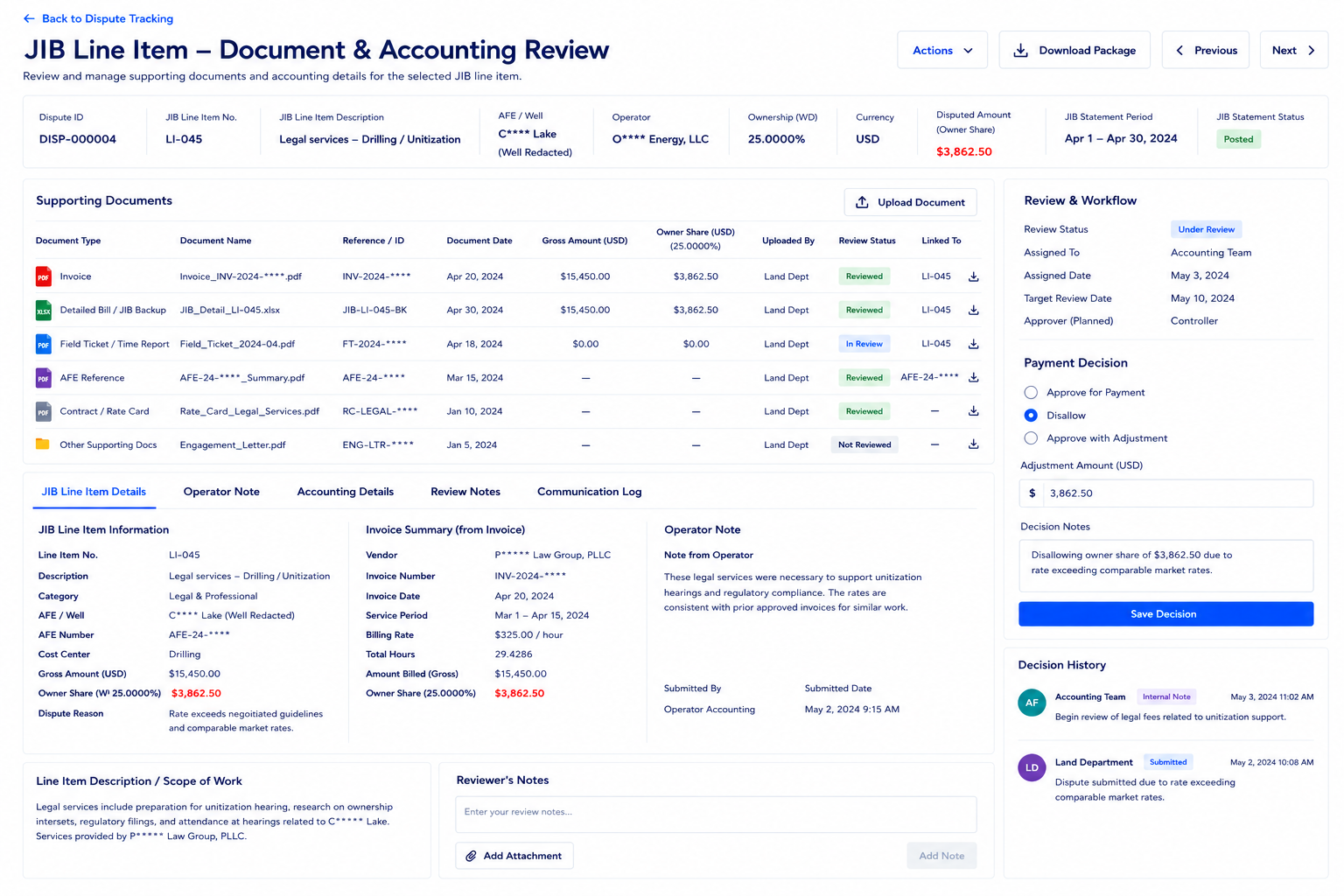

A generic accounting system may let users record a JIB payment as an expense, but working interest owners often need to audit the JIB before payment. That review happens at the line-item level. Each charge may need to be checked against the correct well, lease, operating period, cost category, ownership percentage, AFE reference, and supporting document.

The basic owner share calculation is gross charge × working interest percentage. If a JIB line item shows a $60,000 gross cost and the owner has a 10% working interest, the expected owner share is $6,000. But the real question is not only whether the math is correct. The owner also needs to know whether the gross cost belongs to the right asset and whether the correct ownership basis was used.

Oil and gas accounting software should make those connections easier to review. Instead of entering one total expense, the system should help track line items, support files, review status, payment decisions, and disputes. This is especially important when the owner works with multiple operators and receives several statements each month.

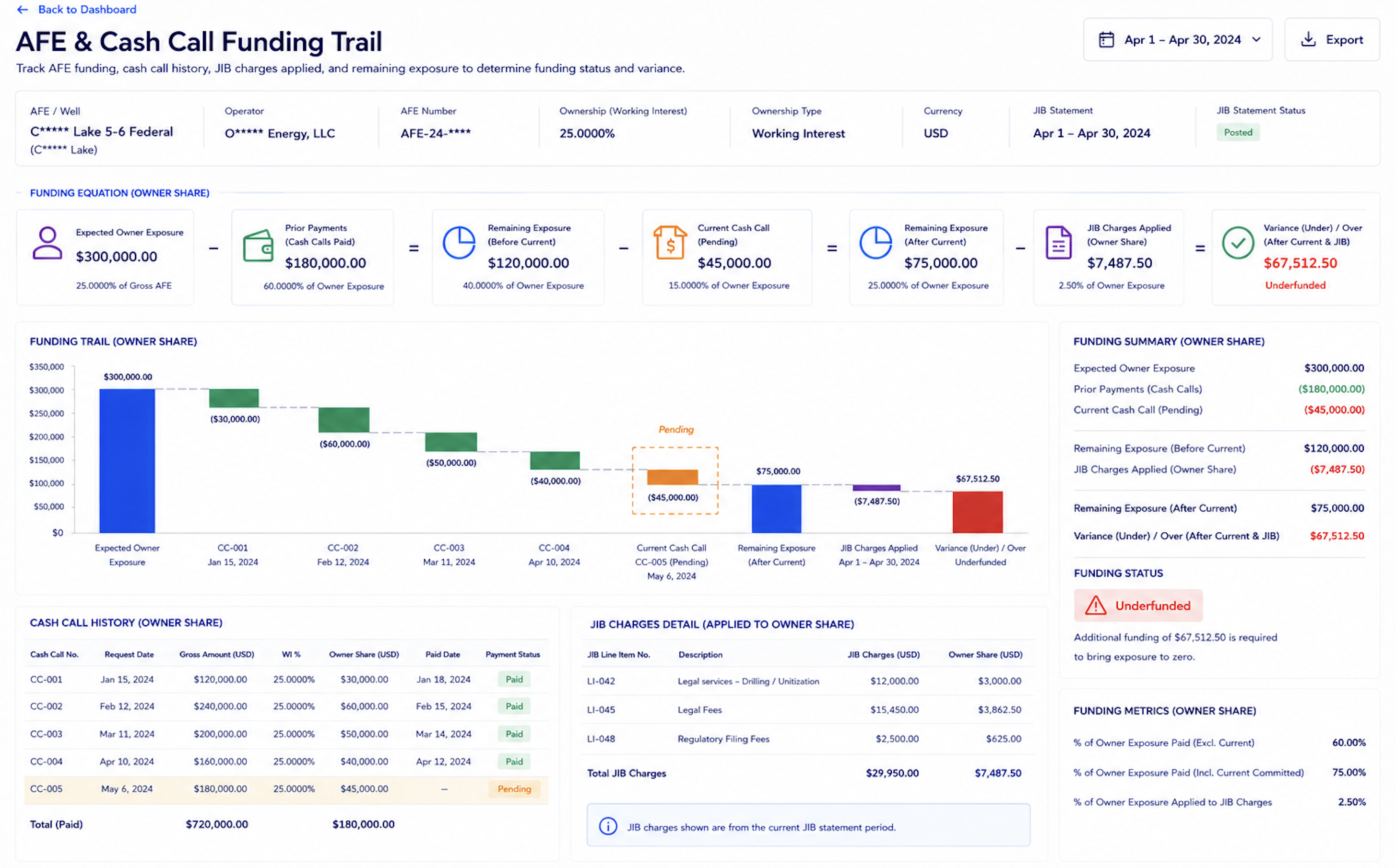

Cash Calls Create a Funding Trail

Cash calls are another area where generic accounting tools can become limited. A cash call may look like a payment request, but for working interest owners it is also part of a funding trail. The owner needs to know which project is being funded, how the request compares with approved AFE exposure, how much has already been paid, and how the amount will later reconcile against JIB charges.

A useful review compares approved gross AFE × working interest percentage against cumulative funding. If an approved AFE is $1,000,000 and the owner has a 12% working interest, expected exposure is $120,000. If the owner has already paid $80,000 in cash calls and receives another request for $55,000, total funding becomes $135,000, which is $15,000 above expected exposure.

A generic accounting tool may record both payments, but it may not automatically show that the owner has crossed the expected AFE exposure. Oil and gas accounting software should help track cash calls, prior funding, remaining exposure, overfunded positions, prepaid balances, and later JIB reconciliation. This turns payment recording into funding control.

Ownership Is Not Just a Vendor Detail

In general accounting, the vendor or payee is often the most important counterparty. In oil and gas accounting, the ownership basis can be just as important. Working interest percentage may vary by well, lease, unit, formation, project, effective date, or participation election. If that ownership context is missing, the accounting record may be complete from a bookkeeping perspective but weak from a review perspective.

For example, if a gross charge is $200,000, the difference between 7.5% and 8.25% working interest is $1,500 on one charge. Across multiple statements or capital projects, small ownership differences can become material. Non-operators need to confirm that the billed percentage matches the correct asset and period before payment is approved.

Oil and gas accounting software should help connect ownership records with JIB charges, cash calls, AFEs, adjustments, and payment status. This helps reviewers identify ownership mismatches before they become repeated billing disputes. It also makes the review more defensible when the operator or internal management asks why a charge was paid, held, or questioned.

Supporting Documents Need to Stay Connected

Generic accounting systems may allow attachments, but oil and gas review often needs documents to be tied to specific operational records. A JIB line item may need an invoice, field ticket, work order, AFE reference, operator explanation, or adjustment note. A cash call may need a project description, ownership basis, prior funding record, and later JIB reconciliation.

If these documents are stored separately, the reviewer may still record the transaction but lose the audit trail. This becomes a problem when a question appears months later. The team may know that a payment was made, but not why it was approved or which support was available at the time.

A stronger system should keep documents attached to the relevant charge, project, AFE, cash call, or dispute. It should also show whether support is complete, missing, requested, or accepted with a note. That status matters because not every missing document means the charge is wrong, but missing support should still be visible.

Reporting Should Explain Exposure, Not Just Totals

Generic financial reports often focus on totals by account, vendor, period, or category. Non-operators need those reports, but they also need views that explain oil and gas exposure. How much has been billed by operator? Which wells have rising LOE? Which AFEs are approaching expected exposure? Which cash calls have not yet been reconciled against JIB charges? Which disputes are still open?

A useful oil and gas accounting report should help management understand both financial totals and operating context. For example, a monthly expense report should not only show that costs increased. It should show whether the increase came from routine LOE, workover activity, capital spending, prior-period adjustment, or ownership correction.

This kind of reporting helps non-operators make better decisions. A cost increase tied to an approved workover may be expected. A cost increase caused by recurring missing support or unexplained LOE movement may need follow-up. Oil and gas accounting software should help separate those situations without forcing the team to rebuild reports manually.

When Generic Tools May Still Work

Generic accounting tools may still be useful for early-stage or very simple workflows. If a working interest owner has a small number of interests, limited monthly activity, few operators, and minimal JIB complexity, basic bookkeeping software may be enough for recording payments and producing standard financial reports. The issue is not that generic tools are bad; it is that they may not carry enough oil and gas context as complexity grows.

The pressure usually appears when the owner receives more statements, joins more projects, reviews more cash calls, or needs better support for management reporting. At that point, the team may begin using spreadsheets, folders, and email notes around the accounting system to fill the gaps. That workaround can function for a while, but it often becomes harder to maintain.

A practical signal is whether the team can answer review questions without searching multiple places. If JIB support, ownership records, AFE files, cash calls, payment status, and operator explanations are scattered, the accounting process may need a more connected oil and gas workflow.

How a Connected Workflow Helps

Software can help. Here’s how Petrofly does it. Petrofly is not just a place to record transactions. It helps working interest owners connect oil and gas accounting activity with the records that explain it: JIB statements, cash calls, AFEs, ownership data, supporting documents, payment status, operator notes, and review decisions.

For working interest owners, Petrofly can help teams:

Unify JIB, cash calls, AFEs, ownership, documents, payments, reviews in one system.

Review charges, interests, shares, adjustments, disputes, balances without spreadsheets.

Track cash calls against AFE exposure and JIB charges to clarify funding positions.

Keep invoices, tickets, explanations, comments, and approvals attached to each record.

Flag missing support, ownership mismatches, AFE overrun risks, open disputes, and unreconciled balances.

Configure fields, workflows, reports, and labels to fit each customer's accounting review.

Support cloud access with no download, so all teams work from the same information.

Simple user experience for records, support, status, and reports.

Responsive support for setup, reports, configuration, and queries.

The practical value is that oil and gas accounting review becomes more connected. Instead of recording payments in one system and explaining them through separate spreadsheets, folders, and emails, teams can keep the financial record and the operating context together. That makes review faster, reporting clearer, and payment decisions easier to defend.

Choose Based on Review Complexity

The decision is not simply generic accounting software or oil and gas accounting software. The real question is how much operating context the team needs to support monthly review. If the owner only needs basic bookkeeping, a general tool may be enough. If the owner needs to review JIB line items, cash calls, AFE exposure, ownership percentages, support files, disputes, and reconciliation, oil and gas-specific workflow becomes more important.

Working interest owners should evaluate software based on the questions they need to answer every month. Can the team explain why a JIB charge was paid? Can it connect a cash call to an AFE and later JIB? Can it validate ownership by project and effective date? Can it track missing support and operator responses? Can management see open items without asking someone to rebuild a spreadsheet? When those questions matter, the software should support more than accounting entries. It should help create a reviewable financial trail.

To discuss how Petrofly can support a more connected oil and gas accounting workflow, contact our team for a focused conversation. Try these review steps in a free Petrofly demo. Don’t just take our word for how automated JIB verification eliminates manual spreadsheet friction; experience the intuitive speed yourself using your own complex operational scenarios. Our hands-on pilot lets your lean back-office team stress-test our data visualization tools before making any long-term vendor commitments.