How Oil and Gas Operators Can Reduce JIB Errors Before Month-End Close

Summary

×Errors Usually Start Earlier

For oil and gas operators, Joint Interest Billing pressure often appears at month-end, but the underlying issues usually start much earlier. A vendor invoice may not be tied to the correct well, a workover cost may be missing its AFE reference, or an ownership change may not have been reflected in the accounting workflow. By the time the accounting team begins generating JIB statements, these issues can surface as rework, adjustments, partner questions, and a delayed close.

The warning signs are usually visible before the billing run begins. Operators often run into the same recurring issues when cost data, ownership data, and approval records are managed across disconnected tools. Common early indicators include:

Vendor invoices without clear well, lease, or field references

Workover costs missing AFE numbers or approval context

Ownership changes that are not reflected in the accounting workflow

Cost categories that do not match the correct billing deck

Adjustments that lack a clear reason or review trail

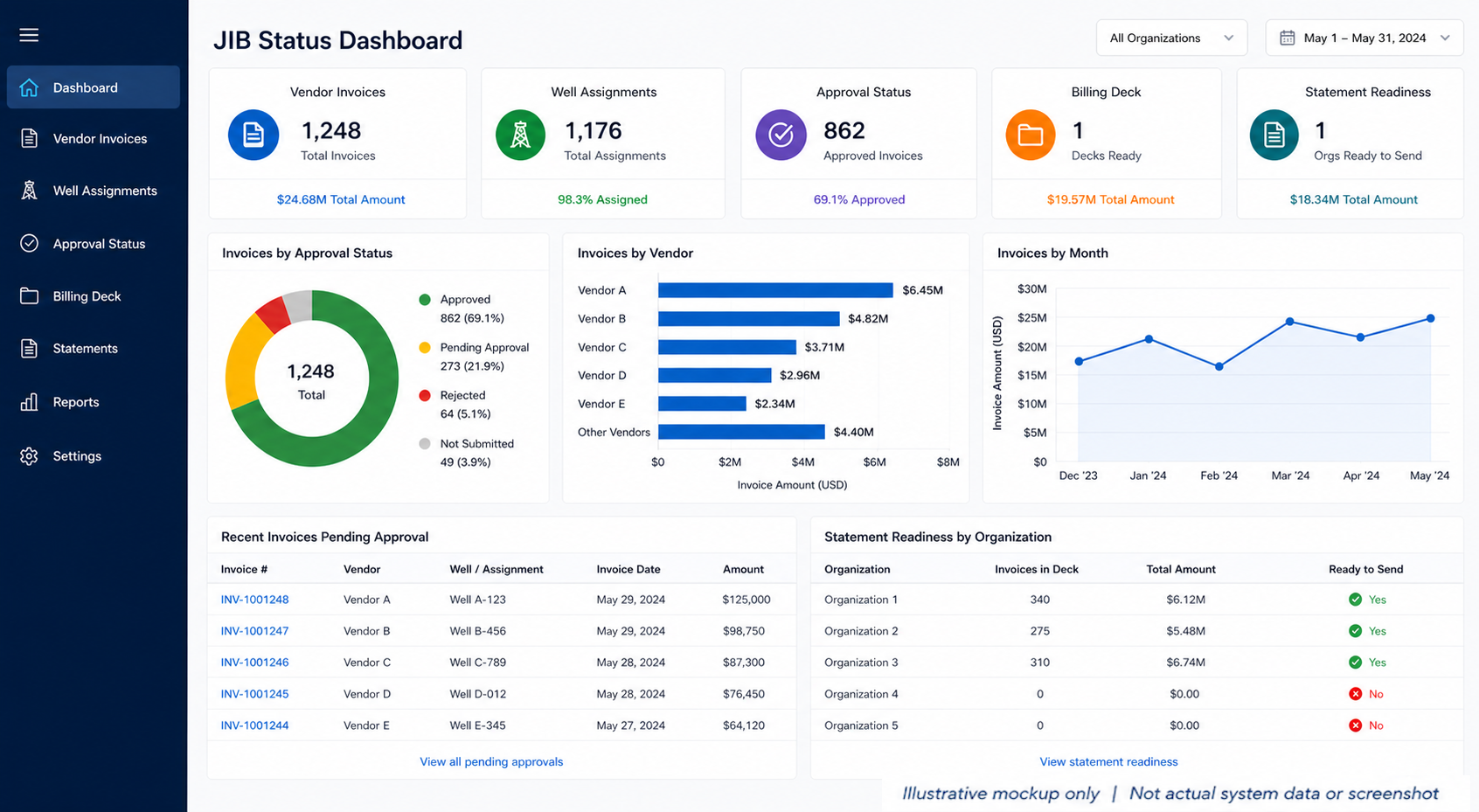

Effective JIB control does not begin when statements are ready to be issued. It begins when costs enter the system, approvals move through the workflow, ownership data changes, and allocation rules are applied. For operators managing multiple wells, leases, and working interest partners, reducing JIB errors means catching problems before they move into statement generation.

Place Field Costs Correctly

Many JIB errors begin with unclear field cost classification. For example, an $18,000 invoice labeled “field service and equipment repair” may require the accounting team to determine whether it belongs to routine LOE, workover expense, capital activity, or an AFE-controlled project. If the record captures only the vendor name and amount, the team may still produce a statement, but the charge will be difficult to explain when a partner asks about it.

Field costs should carry operating context as soon as they enter the accounting workflow. Each record should identify the well, lease, field, production month, expense category, approval status, and supporting notes. Water hauling, chemical treatment, compressor repair, roustabout work, and equipment rental often cross different wells and operating situations, so the earlier the context is captured, the less the month-end review depends on memory and email searches.

A stronger cost record should make the billing logic clear before month-end. At minimum, accounting teams should be able to review:

Which asset the cost belongs to

Which operating period the cost applies to

Whether the cost is LOE, capital, workover, or AFE-related

Who reviewed or approved the cost

Which partners may be affected by the allocation

Do Not Rely on Memory for Billing Decks

JIB allocation is not always a simple calculation based on one fixed working interest percentage. An operator may manage several wells under the same lease, each with different partner participation, while certain ownership changes may become effective in the middle of the month. If billing decks are not managed by asset, period, cost type, and effective date, the numbers may look mathematically correct while the business logic is wrong.

These errors can be difficult to spot internally because the statement may still look complete. The issue often appears when a working interest partner asks why they were billed for a workover they did not participate in, or why costs after an ownership effective date were still allocated under the prior structure. To reduce disputes before close, operators need to confirm that each cost type is using the correct billing basis before statements are released.

Billing deck review should not depend on memory or informal confirmation. Before statements are generated, operators should check whether the allocation basis matches:

The correct well, lease, or asset group

The right ownership period and effective date

The relevant cost type or project category

Partner participation for AFE or workover activity

Any mid-period ownership or participation changes

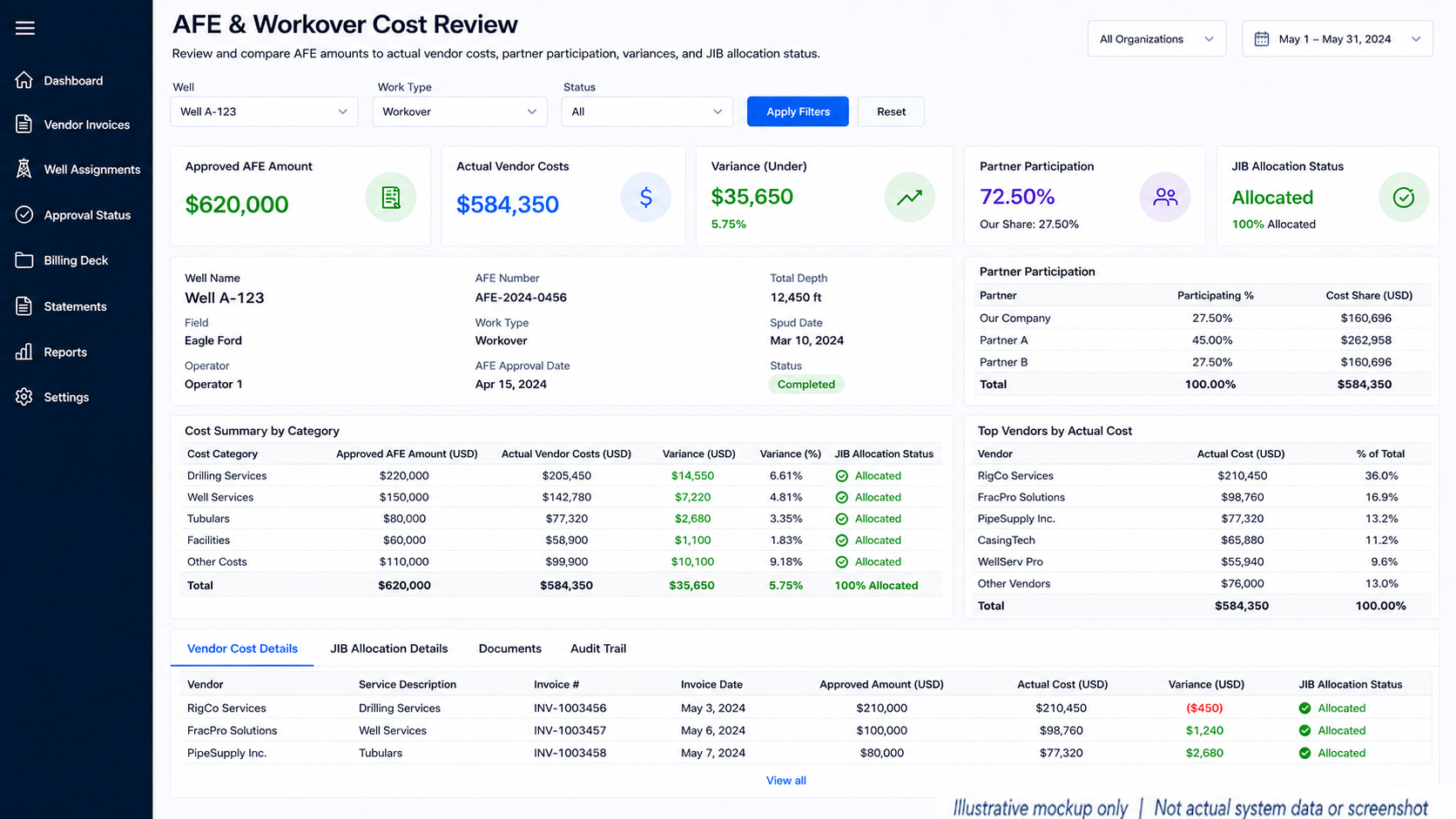

Match AFE and Workover Costs

Workover and capital-related costs are common sources of JIB issues because they often involve approval, budget, partner participation, and later cost allocation. A pump replacement or recompletion activity may have been approved under an AFE, but vendor invoices do not always arrive with complete AFE references. If the accounting team does not connect those costs to the correct AFE during entry, the JIB statement becomes harder to defend later.

This directly affects partner confidence in the billing process. Working interest partners often want to know whether a workover charge was approved, whether it exceeded expectations, and whether it belongs to a project they elected to participate in. Keeping the AFE reference, workover description, approved amount, actual cost, and allocation status in the same cost trail helps reduce month-end explanation work and makes variance review easier.

Make Adjustments Reviewable

JIB adjustments are difficult to avoid in real operations. A vendor may issue a credit memo the following month, a field team may confirm that a cost was assigned to the wrong well, a land team may update an ownership effective date, or a prior-period statement may require reversal and rebill. The problem is not that adjustments happen; the problem is whether each adjustment can be explained.

Consider a chemical treatment charge that was originally allocated to Well A but later confirmed to belong to Well B. If the system simply overwrites the original record, the correction on the next statement may be difficult for a partner to understand. A stronger workflow preserves the original charge, adjustment reason, affected well, affected partners, revised amount, user activity, and statement impact so the accounting team can review the change quickly.

A reviewable adjustment trail should show more than the revised number. It should help the team answer practical questions such as:

What changed from the original charge?

Why was the adjustment created?

Which well, partner, or billing period was affected?

Who made or approved the change?

How did the adjustment affect the current or prior statement?

Find Exceptions Before Billing

Many month-end JIB errors happen because exceptions are found too late. Common examples include invoices entered but not approved, cost categories that do not match the right billing deck, costs without well assignments, incomplete ownership effective dates, or one well’s LOE rising sharply compared with recent months. If these issues are discovered after statements are sent, they can create rebills, payment delays, and partner disputes.

Pre-billing exception review is critical. Accounting teams should check for missing data, unapproved costs, unmatched ownership records, allocation conflicts, and unusual cost spikes before the billing run is completed. For an operator, preventing one inaccurate charge from reaching a partner is often more valuable than producing a batch of statements that later need correction.

Before statements are released, the team should be able to identify:

Costs missing well or lease assignments

Invoices entered but not approved

Ownership records with incomplete effective dates

Cost categories that do not match the intended billing deck

Large cost variances that require review

Prior-period adjustments that may affect partner balances

Answer Partner Questions Faster

After JIB statements are issued, partner questions are usually specific. A partner may ask which well a water hauling charge belongs to, whether a workover cost had AFE approval, why their share increased this month, or when a prior-period adjustment was created. If the accounting team has to search invoice folders, email threads, spreadsheets, and bank records to respond, JIB becomes a reactive explanation process.

Reducing JIB errors also means reducing questions that cannot be answered quickly. Invoice detail, well information, AFE references, billing decks, approval records, adjustment trails, and payment status should be connected. When a partner inquiry comes in, the operator should be able to answer from records and workflow history rather than from memory.

A connected workflow helps accounting teams respond with more confidence. Instead of rebuilding the story behind a charge after the fact, the team can trace the cost from invoice entry to approval, allocation, statement generation, and payment follow-up. This makes partner communication faster, more consistent, and easier to support with records.

Include Recovery Status in the Review

The goal of JIB is not simply to send statements; it is to recover costs. An operator may complete the monthly billing run and still lack a clear view of which partners have paid, which payments are partial, which balances are overdue, and which costs remain unrecovered. If payment tracking is disconnected from the JIB workflow, billing may look complete while cash recovery remains unclear.

Before month-end close, accounting teams should review not only whether statements are accurate, but also which balances remain open and which items are aging. Statement generation, payment received, partner balance, overdue follow-up, and recovery status should be part of the same business trail. This turns JIB from a billing activity into a process tied directly to cash flow discipline and financial control.

For practical review, operators should look at JIB as a full recovery workflow:

Statement generated

Partner balance confirmed

Payment received or partially received

Overdue items identified

Follow-up action recorded

Remaining unrecovered cost visible to the team

Where Petrofly Can Help

Petrofly can help operators bring JIB review earlier into the month by connecting cost entry, well information, AFE references, partner data, approvals, billing status, and payment follow-up in one workflow. Instead of waiting until statements are generated, teams can review exceptions, missing support, and allocation questions before they become month-end rework.

Key support areas include:

Earlier exception control: Identify missing well assignments, unapproved invoices, cost spikes, and ownership mismatches before billing.

Connected JIB records: Link vendor costs, AFEs, billing decks, approvals, adjustments, and partner balances in a clearer review trail.

Modular rollout: Start with JIB, accounting, reporting, or owner relations workflows, then expand as operations mature.

Cloud-based access and configuration: Support team visibility without heavy local infrastructure, while adapting fields, reports, and approvals to actual workflows.

Dedicated post-go-live support: Petrofly’s support team can assist with setup, workflow refinements, reporting changes, and day-to-day questions when JIB issues need faster follow-up.

For operators, the practical value is a more reviewable JIB process that improves control without overbuilding the software environment from the beginning.

Test the Workflow With Real Scenarios

A reliable JIB process cannot be judged only by whether statements can be generated at month-end. Better questions are operational: Can the team catch a misclassified workover invoice before billing? Can the workflow apply the correct allocation basis when an ownership change becomes effective mid-month? When a partner disputes a charge, can accounting quickly find the invoice, approval, allocation, adjustment, and payment history?

Operators can test the strength of their JIB process by walking through real scenarios before month-end pressure builds. Useful test questions include:

Can the team identify costs that are entered but not approved?

Can a workover invoice be matched to the right AFE and partner participation?

Can mid-month ownership changes be reflected in the correct billing period?

Can prior-period adjustments be reviewed without overwriting the original record?

Can partner payment status be reviewed alongside statement history?

Can accounting answer a partner question without searching multiple disconnected sources?

The complexity of oil and gas accounting comes from the intersection of field activity, asset structure, partner participation, and accounting timing. Reducing JIB errors requires turning those moving pieces into a process that is traceable, reviewable, and explainable. For operators, the goal is not simply to generate statements faster, but to make every allocated cost stand up to review.

To discuss how a more controlled JIB workflow could support fewer month-end errors, contact our team for a focused conversation.