AFE vs JIB: Why Working Interest Owners See Cost Differences After Approval

Summary

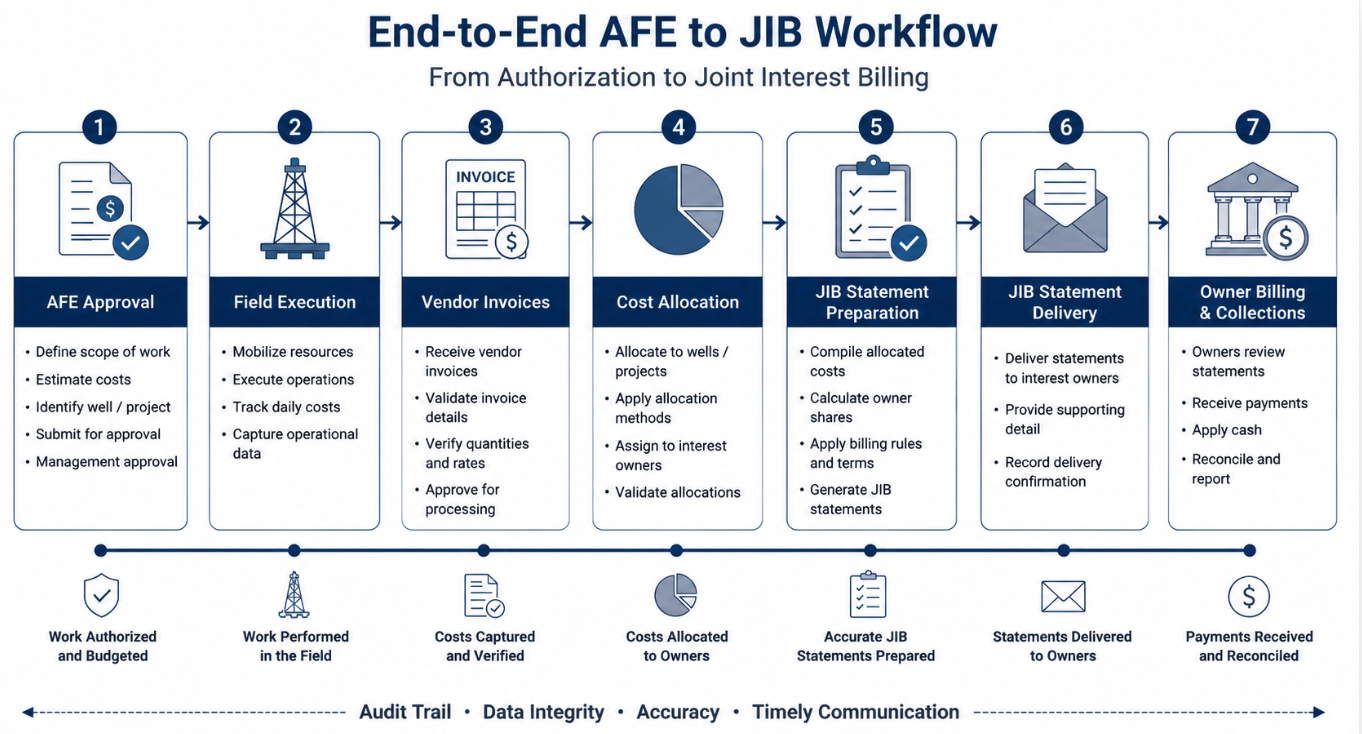

×AFE Is the Plan, JIB Is the Actual Cost

For working interest owners, one of the most common questions after approving an AFE is simple: why is the JIB higher than the amount originally approved? The answer starts with timing. An AFE, or Authorization for Expenditure, is usually prepared before work begins. A JIB, or Joint Interest Billing statement, arrives after work has been performed and actual costs have been allocated.

The AFE gives non-operating owners visibility before capital is committed. It may estimate drilling, completion, workover, facility, equipment, labor, rental, trucking, disposal, or other project costs. The JIB comes later and shows the owner’s share of actual expenses based on the working interest and the applicable operating agreement.

That difference matters because the AFE is built from assumptions. It may rely on expected field conditions, vendor quotes, planned scope, estimated timing, and normal operating conditions. The JIB reflects what actually happened in the field, including invoices, cost coding, operational decisions, weather delays, scope changes, and other execution realities. A clear review process should not ask only whether the JIB is higher. It should ask what changed between the approved plan and the actual cost trail.

The First Check Is the Expected Owner Share

The basic JIB calculation is straightforward. The operator records the gross actual cost, then allocates that cost to owners based on working interest. If the gross cost changes, the owner’s share changes as well. Ultimately, this comprehensive financial control design consistently helps energy companies improve administrative workflow predictability while steadily reinforcing long-term joint venture trust with working interest partners.

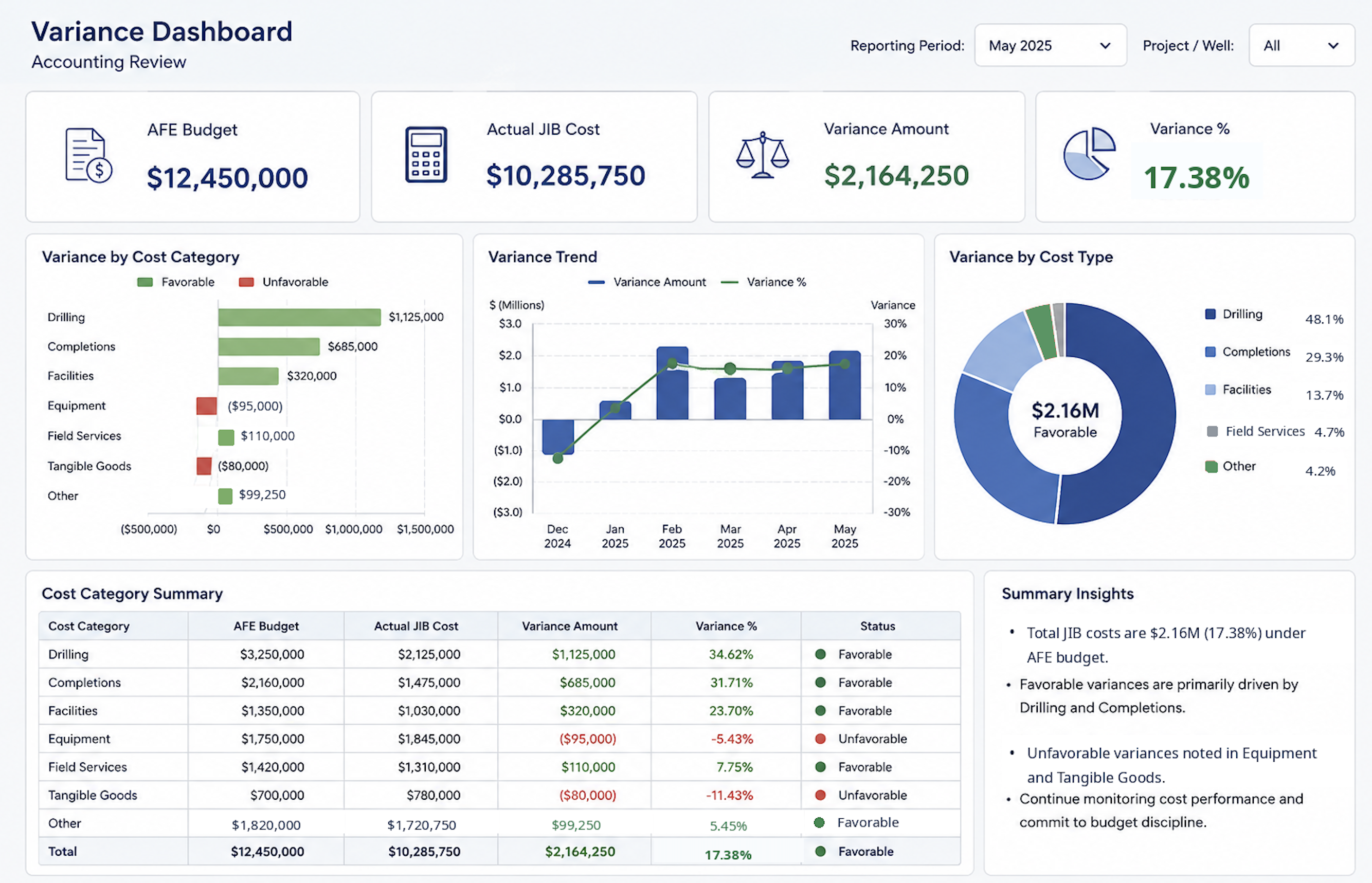

The formula is: Working Interest Owner JIB Charge = Gross Actual Cost × Working Interest Percentage. For example, assume a well completion AFE estimated total gross cost of USD 1,200,000. A working interest owner with a 12.5% working interest would expect an AFE share of: USD 1,200,000 × 12.5% = USD 150,000. If the final actual gross cost becomes USD 1,320,000, the owner’s allocated JIB charge becomes: USD 1,320,000 × 12.5% = USD 165,000. The difference is: USD 165,000 - USD 150,000 = USD 15,000.

That does not automatically mean the bill is wrong. It means the owner needs to understand whether the additional cost is supported by actual field work, vendor invoices, scope movement, cost coding, and allocation logic. Establishing this granular level of forensic verification ensures that joint venture audits are based on transparent ledger reality rather than speculative accounting assumptions.

Variance Should Be Measured Before It Is Questioned

Working interest owners can use a simple variance calculation before raising a question with the operator. This makes the review more objective and helps separate normal cost movement from charges that need follow-up. Implementing this standardized analytical threshold allows joint venture partners to filter out operational noise and focus administrative energy exclusively on high-risk financial anomalies.

Two useful formulas are: JIB Variance = Actual JIB Charge - Expected AFE Share. JIB Variance Percentage = JIB Variance ÷ Expected AFE Share × 100%. Using the earlier example, the variance is USD 15,000. The variance percentage is: USD 15,000 ÷ USD 150,000 × 100% = 10%.

A 10% variance may be reasonable in some field conditions, but it may still deserve explanation if the approved scope was expected to be tightly controlled. Owners should look at both dollar variance and percentage variance. A small percentage on a large project can still create meaningful cash impact.

Cost Differences Often Come from Field Reality

Cost differences often happen because the AFE is prepared before the operator has complete certainty. Field conditions can change, vendor pricing can shift, equipment availability can tighten, and timing can affect labor, trucking, disposal, rental, or service costs. In drilling, completion, and workover activity, even a well-planned job can move outside the original estimate.

Scope changes are another common reason. A recompletion may require additional wireline work. A workover may need longer equipment rental because weather slows the job. A facility repair may require extra parts, trucking, or field labor once the team sees the actual condition. These costs may be valid, but they should be visible enough for owners to understand why the JIB moved.

Not every difference comes from field conditions. Some differences come from coding or allocation. A charge may be legitimate but assigned to the wrong well, wrong phase, wrong cost category, or wrong owner group. That is why owners should not review only the total. They should review whether the cost belongs to the approved project, service period, cost category, and ownership position.

Common sources of AFE-to-JIB variance include:

Field conditions that differ from the original plan

Vendor price changes or equipment availability issues

Added trucking, disposal, rental, or service time

Scope changes needed during execution

Costs coded to the wrong well, phase, or category

Ownership or allocation records that need review

A Higher JIB May Still Be Reasonable

Consider a non-operating owner that approved a USD 900,000 gross AFE for a recompletion project. The owner has a 20% working interest, so the expected share is: USD 900,000 × 20% = USD 180,000. When the JIB arrives, the gross project cost is USD 972,000, making the owner’s share: USD 972,000 × 20% = USD 194,400.

At first glance, the owner sees a USD 14,400 increase and may assume something went wrong. After reviewing the detail, the increase may come from additional wireline work, extra disposal costs, and longer equipment rental due to weather delays. If the operator provides clear documentation and the charges match actual field conditions, the higher JIB may be reasonable.

The same increase looks very different when the detail is vague. If the statement only shows broad categories such as “services” or “operations expense,” the owner has less confidence in the billing. The issue is not only the cost increase. The issue is whether the increase is explainable.

Owners Should Review the Exceptions, Not Every Line Equally

Working interest owners should begin by comparing approved AFE categories against JIB line items. The goal is not to challenge every difference. The goal is to identify charges that fall outside the expected scope, timing, cost category, or project window. This is especially important when a project includes multiple wells, several phases of work, or different cost centers. A drilling-related cost, completion cost, workover cost, or facility cost may all be valid, but each should appear in the right place with the right support. If a charge appears after the expected project window, uses an unfamiliar vendor, or looks duplicated, it deserves closer review.

The strongest review process is usually built around exceptions. Instead of rereading every line manually, owners can focus on large variances, unusual categories, duplicate-looking invoices, unsupported charges, or costs that appear to belong to another well or phase. Deploying this automated exception-driven logic dramatically reduces internal cycle times while sealing the financial leaks that routinely bypass traditional human sampling methods.

Owners should prioritize review items such as:

Large dollar or percentage variances

Charges outside the approved AFE category

Costs billed after the expected project window

Unfamiliar vendors or vague cost descriptions

Duplicate-looking invoices or repeated charges

Costs that appear to belong to another well or phase

Support Should Stay Connected to the Variance

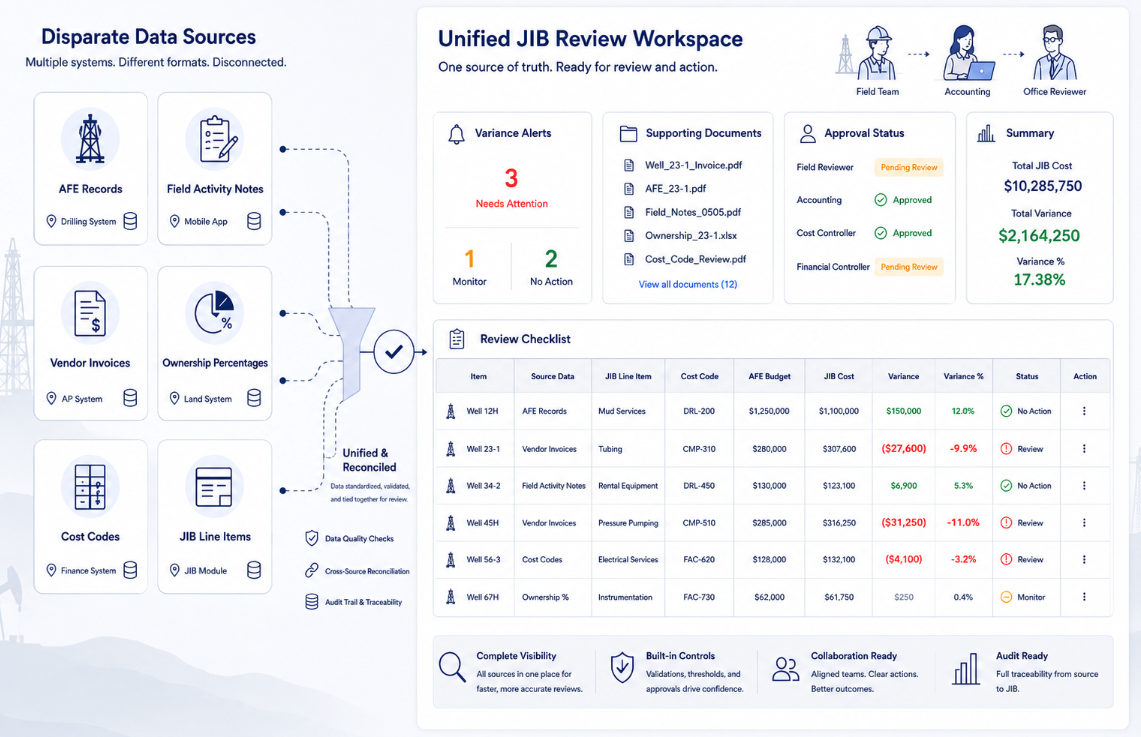

Many AFE-to-JIB questions come from disconnected information. The AFE may live in one folder, field activity notes in another, vendor invoices in another, and JIB statements somewhere else. The cost may be valid, but the story behind the cost becomes difficult to trace. Breaking down these systemic tracking barriers requires a unified data architecture that bridges engineering estimates with actual accounting ledgers to secure a single source of truth.

A stronger review process keeps the AFE, field notes, vendor invoice, ownership percentage, cost code, JIB line item, variance amount, and payment decision close to the same record. This allows the owner to see not only that the cost changed, but why it changed and whether the change is supported.

The strongest rule is simple: do not approve payment for a material AFE-to-JIB variance when the related invoice, cost category, working interest, or field explanation is missing from the review record. This does not mean delaying every payment. It means holding only the variance that cannot yet be explained.

A Practical Review Example

A working interest owner receives a JIB statement with a USD 62,000 charge for a project that had an expected owner share of USD 54,000. The variance is USD 8,000, or approximately 14.8%. Instead of disputing the full amount, the owner compares the JIB line items against the approved AFE categories. The review shows that USD 4,500 relates to additional disposal costs, USD 2,000 relates to rental equipment used for three extra days, and USD 1,500 relates to a vendor charge that appears under the wrong cost category.

The first two items may be valid if they match field records and invoices. The third item may require clarification or correction because the issue is not necessarily the amount, but how the cost was coded. This kind of review gives the owner a stronger position. The owner can approve the supported charges, ask a focused question about the questionable item, and avoid delaying the entire payment cycle. The operator also receives a clearer request and can respond faster.

Management Needs an AFE-to-JIB Variance View

Management does not need only a list of approved AFEs and paid JIB statements. Leaders need to see which projects are running above estimate, which variances are supported, which charges need clarification, and which payments are waiting for review. Equipping executives with this dynamic portfolio visibility transforms static historical reporting into a proactive governance tool that directly safeguards corporate capital efficiency.

A useful AFE-to-JIB variance view should answer:

Which projects have the largest dollar variance?

Which projects have the highest percentage variance?

Which JIB charges fall outside the approved AFE category?

Which costs are missing invoice or field support?

Which charges appear under the wrong well, phase, or cost code?

Which variances are explained by scope, weather, field condition, vendor pricing, or rental time?

Which variance questions are open with the operator?

Which payment decision must be made today?

Without this view, working interest owners react to higher JIB totals after the bill arrives. With it, they can separate supported field variance from questionable billing differences before payment approval. Transitioning to this preemptive validation framework effectively mitigates transactional frictions between operators and non-operators, establishing an institutionalized standard for cost control.

How Petrofly Helps Teams Review AFE-to-JIB Differences

Petrofly can help oil and gas teams make AFE-to-JIB differences easier to review by connecting approved budgets, actual JIB charges, ownership data, cost categories, supporting documents, variance explanations, and payment status in one workflow. Consolidating these fragmented multi-departmental data streams into a single source of truth fundamentally eliminates the systemic information asymmetry that often derails joint venture project lifecycles.

Petrofly supports AFE-to-JIB review through:

AFE-to-JIB visibility: Compare approved estimates with actual charges and supporting cost detail by well, project, category, and owner share.

Variance review: Focus on meaningful differences by dollar amount, percentage movement, cost category, project phase, or payment impact.

Document connection: Keep invoices, approval context, field notes, operator explanations, and payment status close to the related charge.

Ownership and allocation support: Connect working interest, effective dates, owner records, and allocation logic to cost review.

Cloud-based access and flexible setup: Give accounting, operations, management, and authorized reviewers a shared review view, then adjust fields, reports, variance views, and approval steps around actual workflow.

Dedicated support: Petrofly’s team can assist with setup, configuration, data organization, workflow refinements, and post-go-live questions when cost differences need clarification.

Without this structure, AFE-to-JIB differences become scattered explanations across statements, invoices, emails, and spreadsheets. With Petrofly, teams can review supported variances faster, question unclear charges with better context, and make payment decisions with more confidence. AFE-to-JIB variance without control becomes payment friction; connected variance review becomes a clearer path from approved budget to actual cost.

Practical Takeaway

AFE and JIB differences are normal, but unexplained differences create risk. Working interest owners should expect some movement between approved estimates and actual charges, especially when field conditions change. What matters most is whether the JIB provides enough detail to connect the final charge back to the approved scope, actual work, ownership share, and supporting documents.

A strong review process does not need to be complicated. Owners can use simple formulas, variance thresholds, cost-category checks, and supporting documentation to decide when a charge is reasonable and when it needs follow-up. The better the connection between AFE data, field activity, invoices, and JIB statements, the easier it becomes to control costs before payment. For working interest owners, the goal is not to dispute every AFE-to-JIB difference. The goal is to make each meaningful difference traceable, explainable, and ready for a confident payment decision.