Oil and Gas AFE Management Software: What Operators Should Track Before Costs Reach JIB

Summary

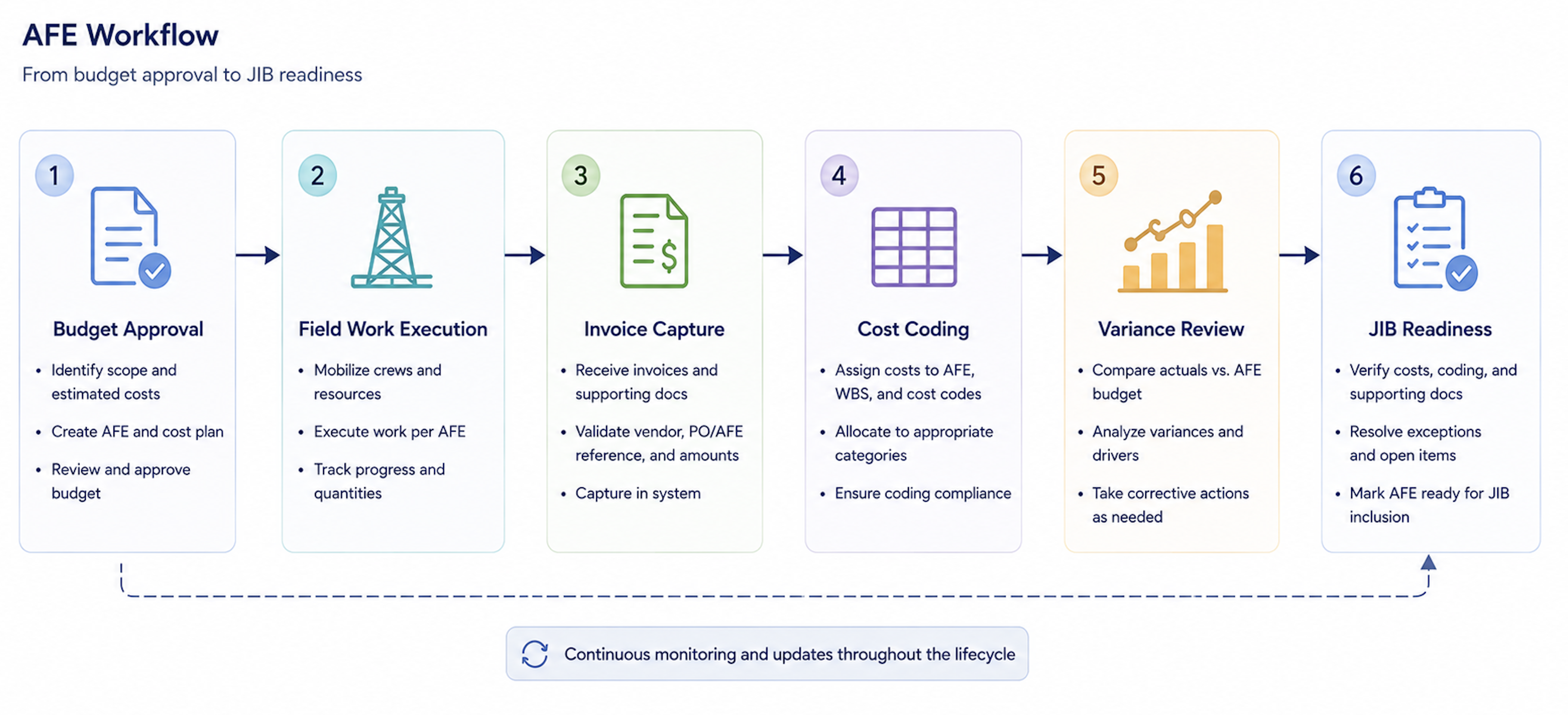

×AFE Approval Is Only the Starting Point

An Authorization for Expenditure gives operators and working interest partners a shared cost expectation before field work begins. It may cover drilling, completion, workover activity, facilities, recompletion, equipment replacement, or other capital and project-based activity. Approval matters, but it does not automatically create cost control.

The real control challenge starts after the AFE is approved. Actual work must be tied back to the approved scope, budget categories, vendor invoices, field activity, cost codes, and ownership participation. If those records are not connected, a valid cost can still become difficult to explain when it appears in a JIB statement.

Many AFE questions appear late in the workflow. A partner may ask why actual costs exceeded the approved estimate, why one vendor invoice was charged to the AFE, whether the cost belongs to the correct well or phase, or whether the operator issued a revised AFE. These questions are easier to answer when AFE data stays connected to execution, not stored as a separate approval document.

Track Budget, Actual Cost, and Variance Together

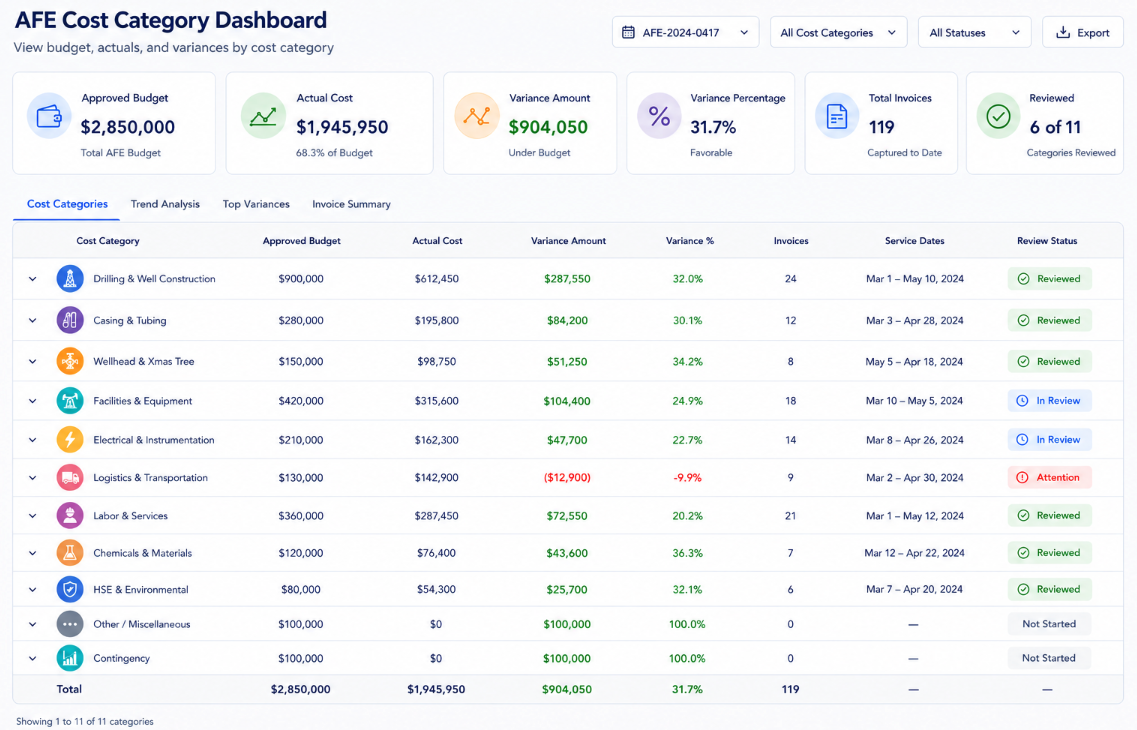

AFE management becomes useful when approved budget and actual cost are visible in the same workflow. The basic formula is: AFE Variance = Actual Cost − Approved AFE Budget. Operators can also use: AFE Variance Percentage = AFE Variance ÷ Approved AFE Budget × 100%. For example, assume a recompletion AFE was approved at $1,500,000. Actual costs recorded to date reach $1,680,000. The variance is $180,000, and the variance percentage is $180,000 ÷ $1,500,000 × 100% = 12%.

A 12% variance may be reasonable if field conditions changed, work took longer than expected, or additional materials were required. It becomes a problem when the operator cannot explain which cost categories moved, which invoices drove the increase, and whether the change was reviewed before billing. AFE management software should help teams see variance by well, project, vendor, cost category, phase, and period before the variance turns into a partner dispute.

Cost Categories Shape the Explanation

An AFE total is not enough for operational control. Operators need to understand whether cost movement comes from drilling services, completion materials, equipment rental, labor, trucking, disposal, supervision, facilities, or other cost categories. Without category-level tracking, a cost overrun becomes difficult to explain.

Cost category structure also affects JIB preparation. A charge may be valid, but if it is tied to the wrong AFE category or project phase, it may create partner questions. For example, a rental charge connected to the wrong phase may not change the total cost, but it can distort budget comparison and make the statement harder to review.

Operators should track:

Approved AFE category and budget amount

Actual cost by category

Vendor invoice and service date

Related well, lease, project, or phase

Field activity note or work description

Approval or change reason

JIB-ready status

Partner participation or ownership basis

Field Changes Need a Review Trail

Field conditions often change after an AFE is approved. Weather, access, equipment availability, geological conditions, vendor scheduling, safety requirements, or production issues may cause the team to adjust work. These changes are not always errors, but they need to be documented in a way finance, management, and partners can understand.

If field explanations stay in emails, texts, or personal notes, they may not be available when JIB statements are prepared. Accounting may see the invoice but not the field reason behind it. Management may see the cost variance but not the operating decision that created it.

An optimized energy workflow routinely ensures that detailed field notes remain permanently anchored alongside the active AFE and its synchronized cost tracking records. By establishing this unified database architecture, operators can guarantee that whenever a project expenditure exceeds the approved budget or falls outside the original scope, the necessary variance justification is captured naturally before the billing cycle begins. Relying on disconnected communication silos frequently leaves back-office accounting teams in an operational vacuum during month-end closes. Maintaining this continuous visibility ensures that every potential discrepancy is fully documented at the point of origin rather than remaining an unexplained line item.

Workover Example: When Variance Is Valid but Needs Support

Consider a workover AFE approved for $900,000. The operator expected a defined scope, but field conditions required additional equipment rental, extra disposal work, and longer crew time. Final actual cost reached $990,000, creating a $90,000 variance and a 10% increase.

The cost increase may be legitimate. The question is whether the operator can support it with field notes, vendor invoices, service dates, revised scope explanation, and cost category detail. If that support is available before JIB generation, the partner can review the charge more efficiently.

If the support is missing, the same cost may become a payment hold, dispute, or repeated clarification request. This is why AFE management should not stop at budget approval. It should support the full path from approval to actual cost, variance explanation, and partner billing readiness.

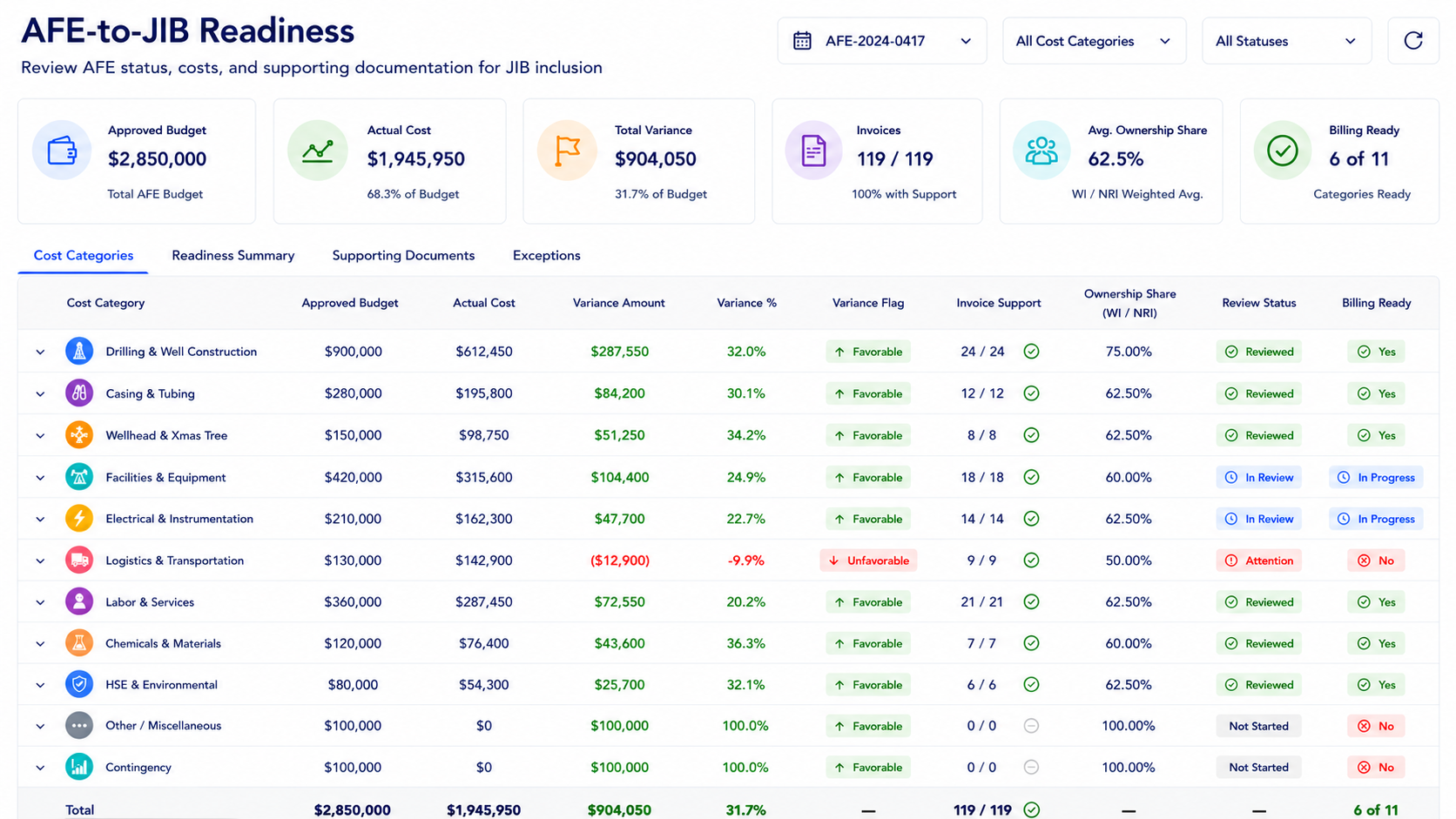

JIB Readiness Starts Before Statement Generation

AFE costs often become JIB questions when the billing record lacks enough context. A partner reviewing a JIB charge may want to see the approved AFE, actual cost, supporting invoice, service date, cost category, working interest, and explanation for variance. If the team has to gather those details after the statement is sent, payment review slows down.

Forward-thinking oil and gas operators generally find it necessary to establish a rigorous validation framework that explicitly defines what makes an AFE-related cost genuinely JIB-ready. Within a dependable financial ecosystem, an operational expense should not automatically advance into the partner billing process simply because a clerk recorded the transaction within the accounting ledger. Relying solely on basic invoice entry frequently introduces tracking gaps that lead to costly downstream disputes and administrative friction during the close. True institutional control requires that every line-item expenditure clears a predefined operational gate before any joint interest charges are distributed to investors.

Before AFE-related costs move into JIB, operators should confirm:

Is the cost tied to the correct AFE?

Does the cost belong to the approved scope or phase?

Is the vendor invoice connected?

Is the service date and work description clear?

Is the cost category specific enough for review?

Does the variance exceed an internal threshold?

Is a field explanation or change note needed?

Is ownership or billing interest current?

Is the charge ready to be explained if a partner asks?

Common AFE Management Mistakes

Operators do not usually lose control because one person forgets to review an AFE. Problems more often come from ordinary workflow gaps. Approved budgets sit in one place, invoices in another, field notes in another, and JIB preparation somewhere else. Common mistakes include treating the approved AFE as the final control record, reviewing only total variance instead of category-level movement, leaving field explanations in emails, and waiting until JIB preparation to confirm invoice support. Another frequent issue is not separating ordinary variance from variance that requires partner explanation. When every difference is treated the same way, teams either over-review small items or miss material exceptions.

A more mature workflow helps teams focus on the right questions. What changed? Why did it change? Is the cost supported? Does it belong to the AFE? Should the partner see an explanation before payment review? These questions make AFE management more useful for both financial control and partner communication.

Where Petrofly Fits AFE Control

Petrofly can help oil and gas operators connect AFE records, cost categories, invoices, field context, approvals, JIB preparation, and reporting in a more traceable workflow. The value is not only storing approved budgets; it is helping teams understand how approved work turns into actual cost.

Petrofly can support AFE control through:

AFE-to-cost visibility: Connect approved budgets with actual field and vendor costs.

Variance review: Track meaningful cost differences before they become partner questions.

JIB readiness: Keep cost context closer to the billing workflow.

Cloud-based access: Give finance, operations, and management a shared review view.

Flexible setup and support: Start with priority AFE workflows, then adjust fields, reports, and review steps around the operator’s process.

Before Costs Reach JIB, Keep the Record Explainable

AFE management software should help operators connect approved budgets with actual execution before costs reach JIB. When AFE records, invoices, field explanations, cost categories, variance review, and billing readiness stay connected, operators can reduce partner questions and explain cost movement with more confidence.

For operators, the practical value is not only knowing whether a project is over budget. It is knowing why the variance happened, which records support it, and whether the cost is ready to be reviewed before it appears on a partner statement. Petrofly can support teams that want AFE control to become part of a more traceable oil and gas workflow. For teams reviewing AFE variance, JIB readiness, or cost control gaps, Petrofly can support a focused workflow discussion.